Economists at DG ECFIN are starting to notice something we have pointed out already some time ago: Despite an enormous cut in wage costs, Greek exports have firmly stayed put in recessionary territory and hopes for an export-led recovery have proven to be illusive. Troubled by this failure of Greek exports to lift off, DG ECFIN economists do what economists do and that is to build an econometric model to find out what exactly is going wrong. The conclusions from their model are quite interesting.

A first conclusion is that the low export performance of Greece is not just a recent phenomenon but is already dating back a long time ago with the volume of missing exports being estimated at around 24% to 33% during the 1995 -2008 period. This dismal performance got further exacerbated under the adjustment program with Greek export performance deteriorating significantly and lagging behind the recovery in other programme countries and with the gap in export volumes having risen to 40.5% in 2009. Here, the paper puts the blame on policy uncertainty and the evaporation of trade credit, the latter resulting from the large outflows of deposits from the Greek banking system.

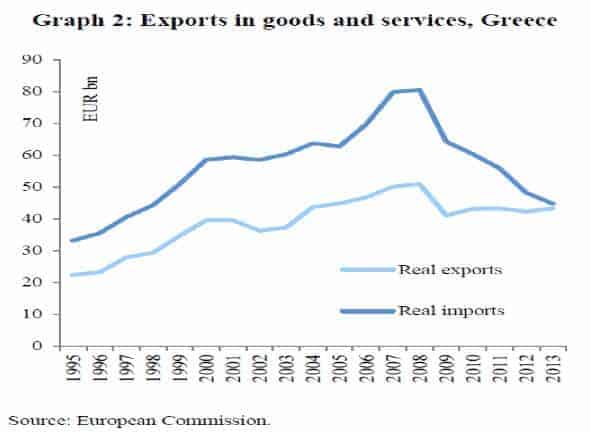

This also implies that the substantial correction of external imbalances that took place has everything to do with import demand collapsing because of the squeeze in domestic demand but has very little or nothing to do with exports increasing (see graph below).

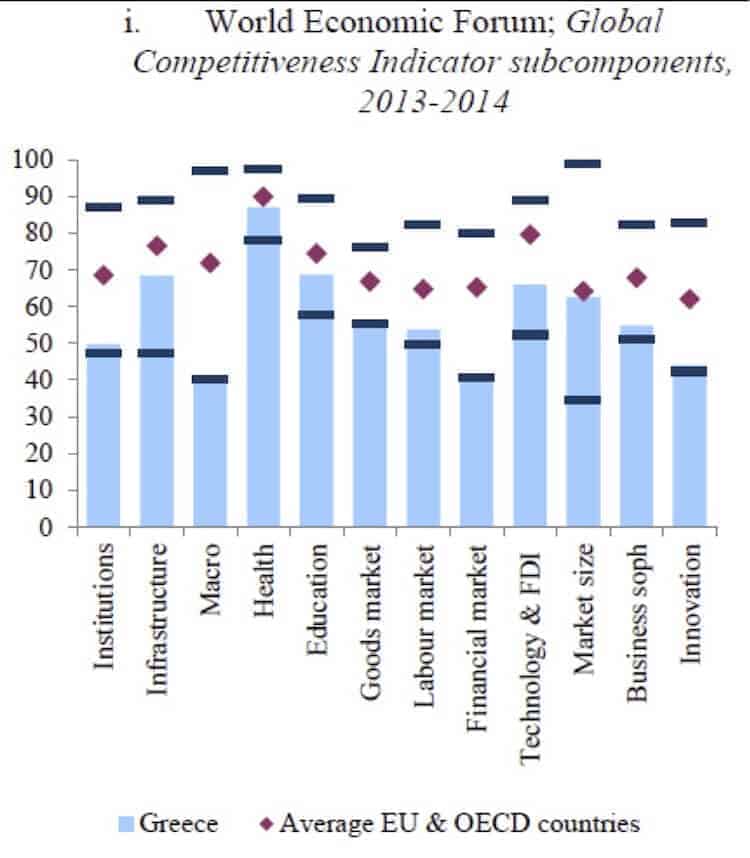

The second conclusion from the model is that this export deficit is caused by an ‘institutional’ deficit, with weak and low quality institutions creating obstacles and difficulties for Greek business to engage in foreign trade. On the basis of four datasets (Global Competitiveness ranking from Wold Economic Forum, World Bank’s Doing Business report, World Bank’s Worldwide Governance Indicators, OECD Sustainable Governance Indicators), the paper finds Greece severely underperforming on a wide range of institutional indicators such as ‘goods market’, ‘innovation’, ‘registering property’, ‘enforcing contracts’, ‘political stability’, ‘macroeconomic environment’, ‘social affairs’, ‘economy and employment’ and ‘financial market’.

Regressions run with the model confirm that about half or even three quarters of the total of missing exports can be explained by the low quality of institutions, with in particular the dimensions of contract enforcement, business sophistication but also political stability, economy and employment as well as the macroeconomic situation playing a key role.

To be noted is that, in all of these regressions, the dimension of wages and wage costs is nowhere to be seen and that the missing export performance of Greece is purely explained in terms of geographical distance, size of the economy and quality of institutions.

Deep internal contradictions in structural adjustment policy

Having the results from this model in mind, it becomes even more clear why the Greek structural adjustment program of brutal austerity and deep wage cuts was doomed to fail from the very start. Austerity, as operated in Greece, has indeed been unprecedented with consecutive rounds of fiscal cuts totalling up to an amount of some 27% of GDP (see here on page 7 for a comparison between countries).

This, in combination with a 15% cut in wages, worked to drag down many of the institutional indicators identified by DG ECFIN’s paper. By triggering a 25% drop in real GDP, by pushing up unemployment to rates as high as 28% and by increasing anchored poverty rates by 15 percentage points up to 35.8% in 2012, the twin policy of austerity has worked to undermine political stability, the macro situation, the state of the economy and employment and, last but not least, the social situation. Any potential effects obtained by changes in wage competitiveness were simply overwhelmed by this setback in what turns out to be key determinants of structural competitiveness.

There is however more. Despite Greece agreeing to a painful program of massive austerity and wide-ranging wage deregulation, the troika failed to deliver in return something the Greek economy desperately needs: A banking sector distributing credit to the real economy, export credits in particular. This failure of the troika’s program to restore the functioning of finance is illustrated by the graph below where it can be seen that Greece in 2013-2014 has the lowest score of all EU – OECD countries on the indicator of financial markets. What this means in practice can be read in this article, describing how Greek business is constrained by cash and unable to access the raw materials from abroad it needs to produce export goods.

No reason for concern?

DG ECFIN economists would of course not be working at DG ECFIN if they didn’t take a relaxed attitude to all of this. And so the conclusions of their paper minimize the collapse in the above mentioned institutional indicators by referring to ‘cyclical’ factors such as lack of trade credit or policy uncertainty and by claiming that these are only producing a temporary delay in the revival of Greek export industry. In other words, the hope is that a stronger rebound of exports reflecting the reforms undertaken will become visible once the economic cycle reverses.

However, presenting the effects of the policy of austerity and deregulation on institutional quality as being temporary is out of touch with reality. After 6 years of recession, the political situation in Greece is anything but stable. Traditional majority parties have rather become minority parties, while support for the extreme right wing movement Golden Dawn has grown significantly. After 6 years of recession, unemployment is at record highs and it will take many years, if not at least a decade, to bring unemployment back to reasonable proportions. After 6 years of recession, the social situation in Greece is alarming. Here, it needs to be questioned whether the relatively good opinion of international business leaders as reported in DG ECFIN’s paper on health and education (see graph above) is indeed accurate. For example, in 2013 half of Greek unemployed (and recall the unemployment rate is at a record high) are no longer covered by public health insurance and the number of people stating that they have insufficient access to health care has gone up by one third (see slide 32).

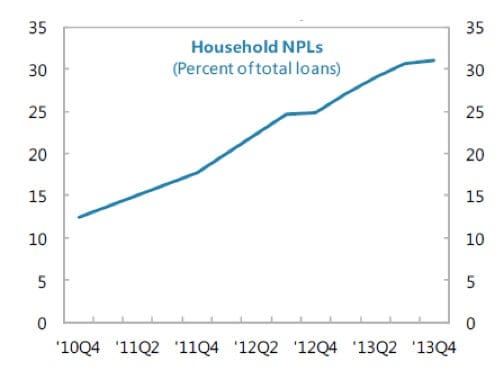

Moreover, the dire situation of Greek banks and their capacity to provide credit to the economy, is anything but solved and there is a vicious, self-reinforcing spiral at work. This spiral finds its origin in the policy of internal devaluation itself, a policy that is now firmly established in Greece with prices and nominal wages falling year after year. The problem with this is that debt burdens are nominally rigid and remain the same even when prices and nominal revenue are falling. In other words, the real burden of outstanding debt increases, making it more and more difficult for households and business to keep up debt payments. This, in turn, leads to a rise in the banking sector’s portfolio of non-performing loans, in the end destroying more banking capital and thereby banks to withdraw more credit flows from the economy. And when banks do get recapitalised, then the troika forces the government to beef up austerity measures. This then results in more deflation, more depression and more loan defaults for the banks. At this moment, Greek banks are facing a mountain of non-performing loans of 31% of outstanding loans, a ratio that continues to rise. (See graph below taken from here and see also here).

TINA and the famous counterfactual

International institutions such as the IMF or the ECB tend to use three lines of defence when faced with criticism. The first line of defence is to simply deny that anything bad ever took place (‘it didn’t happen, collective bargaining coverage did not collapse’). The second one is to admit the occurrence of painful policies but to shift the blame to other actors (‘we didn’t do it, it was the government or the other bail out institution’). The third one is the so called ‘counterfactual argument’, when IMF and/or DG ECFIN do admit to their responsibility of imposing the policy agenda but then claim that things would have even been much worse without these policies. In other words, this is the famous TINA expression of saying that ‘there is no alternative’.

So what would have been the alternative in the case of Greece? The alternative scenario starts with a totally different approach to austerity. Fiscal consolidation was up to a certain degree necessary for Greece, in particular to bring government revenue closer up to a level more comparable with the European average. However, the austerity spiral, by which one round of fiscal cuts simply leads to the next round of consolidation so as to reach the initial deficit targets despite the deepening of the growth depression, should have been avoided. In the same vein, instead of declaring war on collective bargaining, trade unions and minimum wages, policy should have taken a “hands off’ approach here and should have stayed clear from undermining the system of wage formation.

More flexibility in the strategy of fiscal consolidation, together with respect for collective bargaining institutions, would in turn have opened up much more possibilities for social dialogue. Instead of social partners being confronted with a troika dictating what they should be doing and then imposing its own measures anyway, this more flexible approach to fiscal consolidation would have given opportunities to social partners to bargain on trade – offs, basically exchanging a moderation in wage dynamics (not wage cuts!) with the possibility of co-shaping fiscal consolidation policy. The latter with the aim of protecting key areas of social protection and public services as well as to provide fiscal space for growth and job-enhancing policies. This “quid pro quo” would, of course, not at all have been to the liking of the troika because it simply does not fit into their framework of “economic efficiency”.

However, and has been shown by DG ECFIN’s paper discussed here, this framework is simply too narrow. It’s not just deficit or wage numbers that count, issues such as political stability and the social state of affairs also determine outcomes, including changes in competitive position. So the alternative would have been to have a policy program with much less austerity and no wage and social deregulation but at the same time a program that has more chances to work because being supported by a social consensus on the measures to be taken.

The third pillar of an alternative policy scenario is to repair the channel of finance. From the moment it was clear that Greece was serious about engaging with fiscal consolidation policy, the ECB should have stepped in by sending a clear signal to financial markets to stop the speculation against Greece. This signal did finally come in the summer of 2012, when Draghi promised ‘to do anything it takes’. By that time however the Greek adjustment program had already run for two years and much of the damage had already been inflicted. Moreover, even today, the interest charged on Greek sovereign debt is still too high compared to the low rates of nominal growth, implying that the public debt ratio continues to be pushed upwards.

Besides earlier and more convincing ECB action, troika policy should have also tried to repair the financial channel directly by making special credit lines available for purposes of exports and investment. Instead, the focus was limited to on general and costly recapitalisation schemes to save existing banks and their shareholders. Here, certainly the IMF should have known better since exactly the same problem appeared in the Asian financial crisis of the mid-nineties. There, the IMF also imposed brutal cuts on public spending and wages, hoping to see export revival taking up the slack. However, like in Greece no such thing happened until finally Japan stepped in and started to provide export credit finance to the South East Asian countries. It is discomforting to learn that, fifteen years later, this lesson has already been forgotten and that the same mistake of imposing wrong measures (brutal austerity) while forgetting about the necessary help (finance for growth and exports) is being repeated.

Would this alternative policy scenario have cost more? The answer is undoubtedly ‘yes’. Europe would have had to mobilize not just a couple of billions to lend to Greece so that Greece could keep up with honouring its debt service (which itself is to a large extent owed to the banks of the same member states providing these emergency loans). On top of that, the credits for trade and investment, along with additional deficit levels, would have needed to be lend to Greece. So ‘yes’, it would have been more expensive but, at the same time, Greece would have had a program that worked. It doesn’t have such a program right now.