Year of Referendum Disasters

In 2016 the European Union both as an organization and hope for a better and more peaceful future suffered at least two serious and possibly mortal blows: the British “in/out” referendum gave a direct hit, while the constitutional plebiscite five months later in Italy delivered a glancing blow that might yet prove fatal if it leads to an “in/out” on membership of the euro zone (Italexit). With Marine Le Pen promising a French plebiscite should she take power (Frexit), the elites that mismanage the EU must bitterly rue this national scope for direct democracy.

Unlike the seemingly insoluble refugee crisis, the anti-euro political forces in Italy and France have at least clear cause: stagnant economies. The evidence suggests that membership of the euro zone carries a deflationary, low-growth bias.

Looking at the Numbers

The rise of anti-Brussels sentiment reflects a growing perception that economies and the people who work in them would fare better outside the euro zone than in. Key indicators provide support for that perception.

To inspect the “euro effect” I divide the EU-27 (without late-comer Croatia) between countries in and out of the euro zone, assessing their economic indicators since the 2008 global recession. Three of the 19 currency union countries adopted the euro after 2009 – Estonia (2011), Latvia (2014) and Lithuania (2015). I include them with the other 16 because joining the currency union meant their pre-euro economic policies had to closely adhere to euro zone rules for most of those eight years.

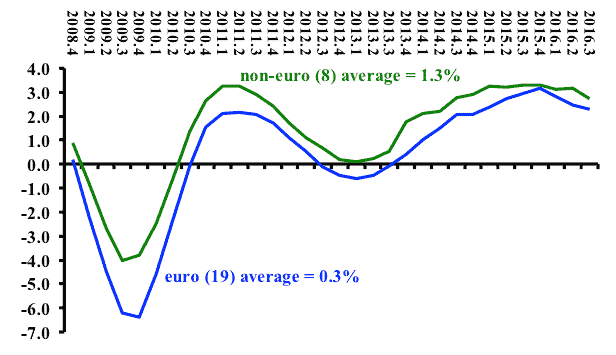

The chart below shows growth rates across countries from the outset of the economic collapse of 2008 through the third quarter of 2016), using a moving average to eliminate purely seasonal effects. Over those eight years, the average growth rate in the 19 was consistently lower than for countries with national currencies.

EU countries, Euro Zone (19) and non-Europe Zone (8), GDP Growth Rate, 2008-2016

Note: Annualized four quarter moving average (each quarter compared to same quarter previous year).

Source: Eurostat

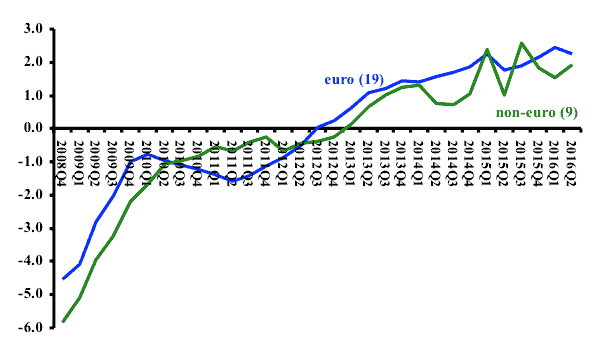

While the governments of some non-euro countries pursued austerity or “fiscal consolidation” policies none did so with the zeal of euro zone governments, frequently in response to pressures from the European Commission and the German government via finance ministers (“Eurogroup”).

The less austere non-euro countries had consistently higher fiscal balances (see below). The average balance across euro countries rose above the Maastricht minus three percent in the second quarter of 2014, two years after the non-euro average. The higher rates of growth shown in the first diagram were one major reason for the lower deficits in these eight countries.

The averages for the euro countries are inflated by extreme single-quarter values for Ireland (25% of GDP in 2011Q3), Slovenia (40% in 2013Q4) and Cyprus (25% in 2014Q1). These very large deficits resulted from bank “bailouts”. Membership of the euro zone meant that these governments could not finance bank recapitalization through their central banks borrowing from themselves, which would have avoided the heavily conditional Troika-type loans programmes.

EU countries, Euro Zone (19) and non-Europe Zone (8), General Government Fiscal Balance, 2008-2016

(percentage of GDP)

Note: Four quarter moving average.

Source: Eurostat.

In recent years, the Commission has placed heavy emphasis on achieving EU “competitiveness”, a term that appears frequently in EU treaties. For example, Article 3 of The Treaty on the European Union describes a “highly competitive social market economy” as a central policy goal. Inspection of the treaties, protocols and statements by EU officials shows “competitive” to mean “export competitive”, with the external current account the accepted yardstick.

Statistics on national current accounts indicate little difference between euro and non-euro countries (see chart below). Over 2008-2016 the current account as a share of GDP averaged zero for the euro countries and -0.3% for the non-euro EU members. Since 2010 the two groups have almost the same outcome, 0.5 and 0.4, respectively.

If current account surpluses are the appropriate measure of “competitiveness”, non-euro countries can considerably more easily increase them. They can devalue, while euro zone countries must reduce nominal production costs. In practice lowering production costs requires wage repression.

EU countries, Euro Zone (19) and non-Europe Zone (8), Current Account, 2008-2016

(percentage of GDP)

Note: Four quarter moving average.

Source: Eurostat.

The preamble to the TFEU pledges the member countries to achieve “convergence of their economies”. While some officials and politicians may interpret this narrowly to refer to the Maastricht “convergence criteria”, the Treaty clearly refers to a much broader vision, as explained by Philippe Monfort in a 2008 EU working paper:

The Treaty establishing the European Community defines economic and social cohesion as one of the main operational priorities of the Union. Cohesion is to be achieved mainly through the promotion of growth-enhancing conditions and the reduction of disparities between the levels of development of EU regions and Member … (P3).

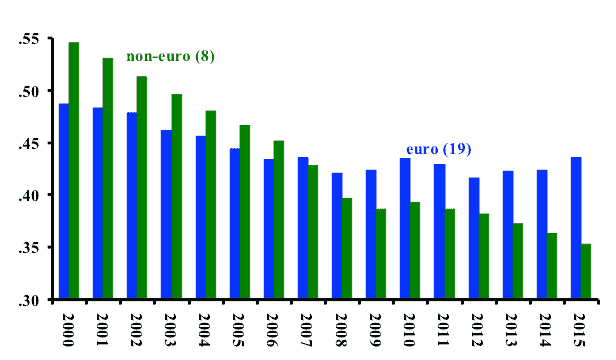

It is relevant to ask whether the introduction of the euro has facilitated this treaty goal of convergence of levels of development. The final chart suggests not. It shows the relative difference in per capita incomes for the EU-27 as measured by the coefficient of variation within each of the two groups, euro and non-euro.

Over the 16 years 2000-2015, the variation among the non-euro countries steadily declined. For the 19 euro zone countries the variation declined 2000-2008, changed very little for the next two years, then, with the introduction of austerity policies in 2010-201, began to rise, returning to its level of ten years before. Even more striking, from 2007 onwards the distribution of per capita incomes became less unequal among the non-euro countries and more unequal in the euro zone.

EU countries, Euro Zone (19) and non-Europe Zone (8), Convergence & divergence in per capital GDP, 2000-2015

(Coefficient of variation)

Notes: Per capita GDP measured in “purchasing power parity”. The coefficient of variation is the standard deviation of per capita incomes divided by the mean (“average”). World Bank statistics used instead of Eurostat because former reports absolute levels and latter does not.

Source: World Bank.

What is the Problem?

Over the last decade the differences between euro and non-euro countries become increasingly obvious and arise from the EU’s singularly dysfunctional treaty-based economic rules, most obviously the fiscal rules.

In practice, the power of the Commission to enforce those rules drastically weakens at the border of the euro zone. With no provision for expelling a member state in EU treaties, the governments of non-euro countries can and do comply with EU rules to the extent they find it politically convenient (Britain and Denmark have explicit opt-outs).

Looking back at the referendums of 2016 and forward to elections this year, it becomes increasingly clear that a central flaw undermining European unity and the EU itself is the common currency. The EU requires democratic reform. The euro and the many rules and restrictions associated with it are an insurmountable barrier to that reform.