Getting Stupid Capital Flows Off The Hook

The analytical note on the next steps for better economic governance that was published mid- February during the informal European Council reopens the discussion on how to obtain a strict coordination of national economic policy making in the Euro Area. Or, to put it more bluntly, how to provide the authorities at European level with the power to intervene in national economic policies.

To underline the necessity of this transfer of competence, the analytical note describes the roots of the crisis in the euro area. Here, the note, written by the four presidents (president of the Commission, the ECB, the Council and the Euro group) excels itself in its efforts to claim that the euro crisis is basically caused by rigid labour and product markets. If, the argument goes, these markets had been more flexible, then supply would have been able to keep up with booming demand. There would have been no explosion in wage hikes reducing the competitiveness of the so called ‘deficit’ countries. Nor would the latter have seen their current account deficits soaring and there would have been no need to indebt themselves in order to finance these record external deficits.

Dubious Graphs

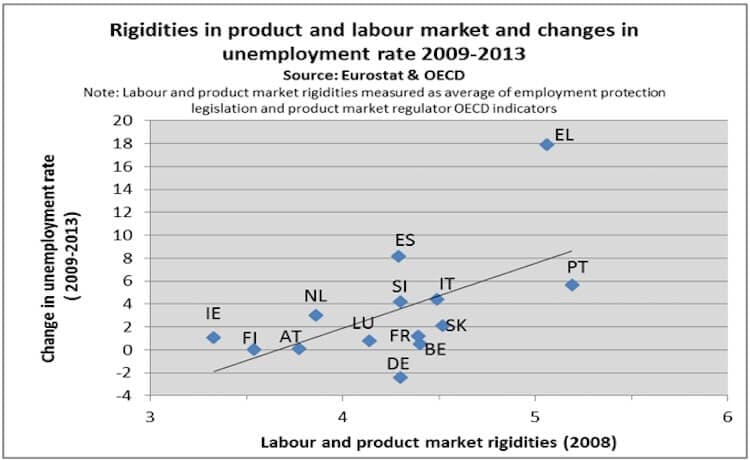

To back up their case, the analytical note presents a couple of graphs that are meant to prove that labour markets in the ‘deficit’ members of the Euro Area are ‘rigid’ and that it is this rigidity which is responsible for the crisis and for record unemployment levels. Below is the first graph that appears in the analytical note, showing a strong correlation between the level of labour and product market regulation in 2008 and the change in unemployment from 2009 to 2013 in a sample of 14 members of the Euro Area.

The message from the graph – that labour and product market rigidities carry with them a heavy price in terms of unemployment – seems clear.

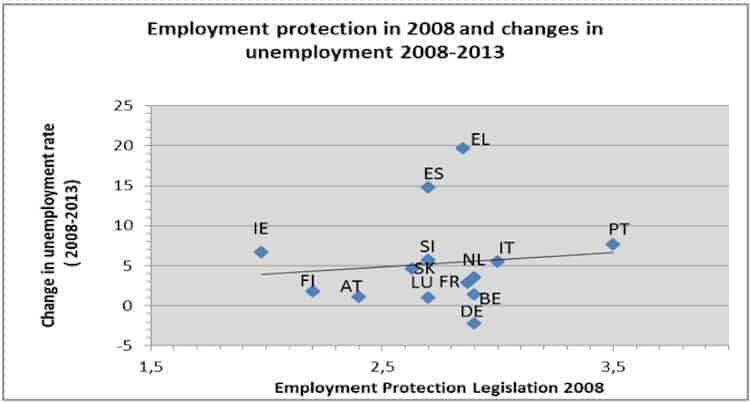

Or is it? Indeed, a closer look reveals that there’s a reason why the analysis paper is using an indicator that combines both the level of labour market rigidity as well as the level of product market rigidity. When looking at the specific link between labour market rigidities and changes in unemployment, we get a totally different picture. (We have used the identical set of countries here).

The strong relationship between market rigidities and unemployment performance that could be observed in the first graph now disappears and is replaced by a correlation that is hardly noticeable. Moreover, there is a lot of variation around the trend line. In particular, and this should constitute something of an enigma for the thesis of the “presidents’ paper,” there is the fact that Germany has managed to get unemployment down while Spain has seen unemployment soar and all of this despite the fact that job protection is at a similar level in both countries. If rigid job protection is so detrimental for unemployment, then why has unemployment in Germany gone down substantially?

Wages And Capital Flows: Getting The Direction Of Causality Right

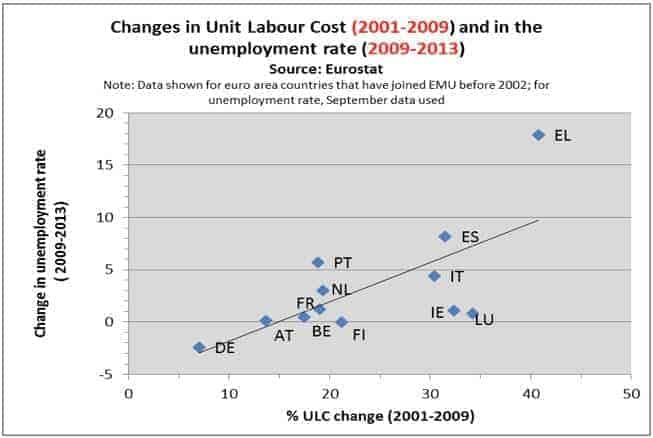

A second graph from the analytical paper, which is even more dubious, suggests that increases in wage costs are directly causing unemployment to go up and even to go up substantially. It also suggests that if we want to get unemployment down, we need to depress wages.

There is, however, something peculiar about this graph. To be able to show this strong correlation between wage costs and unemployment, the graph above is using two different time periods. Changes in unemployment AFTER the financial crisis are being compared with increases in unit labour costs BEFORE the crisis. In other words, this is a bit like comparing ‘apples with pears’ since recent trends in unemployment are being associated with trends in wage costs that took place some ten years before!

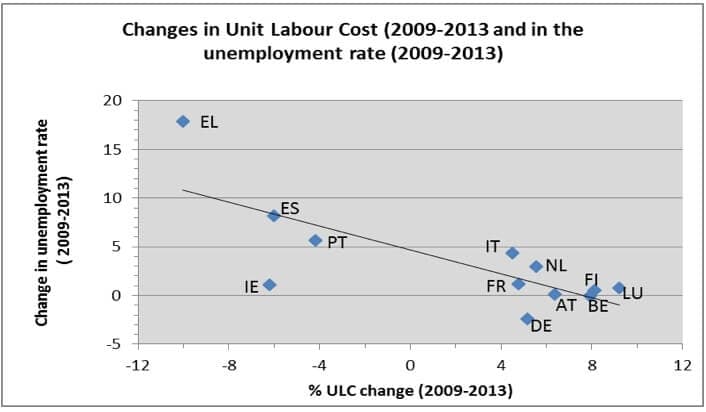

When repeating an identical exercise but this time with changes in unit labour costs and changes in unemployment for the SAME period, the picture becomes quite different. This alternative graph (see below) is now showing a strong NEGATIVE, not a positive correlation. Cuts in wage costs are now correlated with rising unemployment whereas robust increases in wages go hand in hand with falling rates of unemployment. This graph clearly tells the story of what is actually happening in reality. It tells the story of the failure of the strategy of internal wage devaluation to trigger recovery, producing more recession instead. It also tells the story of Germany shifting course since the start of the financial crisis, away from wage depression and deregulation towards “Kurzarbeit” (keep employees on board with short-time working instead of firing them) and towards a renewal of collective bargaining and wage dynamism.

Finally, let’s return to the initial graph using the two-period comparison from the analytical note. What is happening here is that there is a third force operating in the background and driving the two trends of rising wage costs as they occurred ten years ago and recent increases in unemployment.

Capital flows in the single currency constitute such a force. During the first ten years of monetary union, massive capital flows, originating from the core Euro Area countries’ strategy of competitive disinflation, have been feeding into asset prices and debt-driven booms of other Euro Area members, thereby overheating the economies of the latter and pushing up inflation. To maintain purchasing power in the face of rising inflation, nominal wage dynamics in the latter countries had to follow, hence the major hikes in wage costs over the 2001-2009 period.

Debt and asset price booms, however, cannot continue endlessly. Sooner or later, there comes a moment when the dynamics of the financial cycle turn around and a finance-driven boom becomes a bust. That moment came with the crisis of the euro in 2009 when financial markets, fearing they had already lent out too much capital, refused to continue recycling the savings surpluses from the Euro Area core to the periphery. From that moment on, Euro Area members such as Greece, Spain, Portugal, Ireland and later Italy were confronted with a major ‘financial sector strike’ while at the same time being saddled with an enormous mountain of mostly private sector debt. The consequence is that their economies collapsed and unemployment rose enormously.

The real force driving all of this is not reckless wage dynamics but irrational capital flows, first luring economies into indebting themselves enormously, then staging a ‘sudden stop’ that pushes the economy into profound recession. Wages, meanwhile, are simply a ‘side show’ with rising wage dynamics being the result of massive capital inflows and not the other way around. Numerous studies, from the IMF, the Commission and even from the ECB itself indeed come to the conclusion that the ‘signature’ of Euro area external imbalances is financial and that wages and falling export competitiveness have little to do with it.

Conclusion

The four presidents’ note once again testifies to the danger of European economic governance being grabbed by “the powers that be” and doing so with the aim of pushing through their ideological choice in favour of a ‘free market’ Europe.

In the end, their analytical paper boils down to yet another attempt to obscure the fact that financial flows originating from the ‘creditor’ countries got completely out of control during the first decade of the Euro. Instead, the analytical paper openly shifts the blame for the crisis on labour market institutions that promote workers’ rights. Trade unions and progressive politicians would do well to clearly say ‘no’ to this flawed and biased approach.