Tax policy in the European Union is based on a fundamental and as yet unresolved tension between the common internal market and 27 different tax systems. The internal market guarantees the free movement of capital but tax enforcement essentially ends at national borders. At the same time, the member states are driven into organised tax competition, which undermines their fiscal sovereignty.

This leads to revenue losses in a period of unprecedented global challenges, from climate change to the Covid-19 crisis. The current fiscal patchwork is not an option to make Europe strong in the world. The principle of fair taxation must become the standard in the EU.

Active assistance

In the first quarter of 2020, five member states already had a national debt greater than their gross domestic product, including two large founding states, France and Italy. At the same time, global corporations are withdrawing from tax collection: in 2011, Apple made profits of €16 billion in Europe yet paid just €50 million in taxes to the Republic of Ireland, where all these profits were booked.

This ‘tax bargain’ was made possible thanks to the active assistance of the Irish tax authorities, which provided Apple with an attractive tax-saving scheme. To add insult to injury, in July a ruling by the Court of Justice of the EU relieved Google of an additional tax payment of €13 billion which the European Commission had directed in 2016.

Amazon’s operating profit in 2018 was around €11 billion but between 2003 and 2014 the company did not pay tax on 75 per cent of its EU sales. This was made possible through a preliminary tax assessment agreed with the Luxembourg tax authorities. In the United States, the Amazon group even received a tax credit of $137 million.

Shifting burden

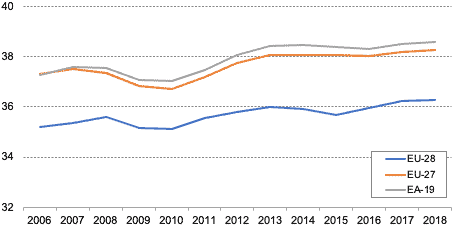

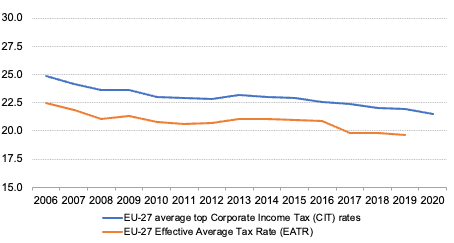

It is unsurprising companies take advantage of the peculiarities of tax systems for their aggressive tax planning, while formally adhering to ‘the letter of the law’. The principle of fair taxation of citizens and companies is thus a receding horizon. The graphs below show how the burden of taxation has shifted from corporations to labour in recent times.

Implicit tax rate on labour, 2006-18 (%)

Nominal and effective corporate tax rates (%)

As a result, economic disparities between and within member states are widening, fuelled by the Covid-19 pandemic. In its Action Plan for Fair and Simple Taxation to Support the Recovery Strategy, the European Commission affirms that tax fraud and evasion pose a threat to public finances and that member states ‘today more than ever need secure tax revenues to invest in the people and businesses that need them most’.

This is however tantamount to conceding that EU packages of measures, such as the directive to combat tax avoidance, have remained largely ineffective. Indeed the loss of revenue by member states due to international tax evasion was estimated in 2016 at €46 billion for income, capital-gains, wealth and inheritance tax, and in 2017 at €137 billion for value-added tax. In addition to tax-avoidance offers, tax competition is taking place among member states for company settlements with regard to corporate-tax rates: these range from 9 per cent in Hungary to 34.4 per cent in France.

Real solution

With fair burden-sharing thus undermined and fair competition frustrated, 74 per cent of EU citizens believe urgent action must be taken against tax avoidance and evasion. However, the European Commission’s ambitious agenda to tackle tax avoidance with the help of state-aid law, opening proceedings against Apple, Google, Fiat Finance and others, often fails because of insufficient evidence. The procedural route is not a promising option—a real solution can only be found through joint, European and global, regulatory efforts.

Is anything new and revolutionary possible within the framework of the Treaty on the Functioning of the EU? Article 113 provides for unanimity in the Council of the EU for the harmonisation of indirect taxes. This is probably one reason why there exists only one harmonised minimum tax rate in the EU—for VAT—and this dates back to 1993. The pandemic and empty state coffers could set the ball rolling again for reform.

The tax legislation of the last century is based on the principle that profits are taxed at the place of value creation, starting from the physical presence of a company. This model is being undermined by globally operating corporations, through profit shifting within the corporate structure. Digital business models, which are largely based on intangible assets, are currently taxed differently or not at all. The commission presented two legislative drafts for the taxation of the digital economy as early as 2018.

Digital taxation

The first initiative concerns the taxation of digital companies. It aims to harmonise tax rules for companies with a significant digital presence in the internal market. Profits should be registered and taxed where interactions between companies and users take place via digital channels. In addition, the draft directive on the Common Consolidated Corporate Tax Base is supposed to be extended to include a tax connection point for digital business activities.

This would be a first step towards an EU-wide, harmonised approach to recording tax incidents. Profits are allocated to those member states in which subsidiaries are located or in which a digital presence is established.

The second proposal is for a transitional tax of 3 per cent of turnover for the provision of digital services by multinational companies. It is estimated this ‘digital tax’ could generate revenues of €5 billion per year.

These proposals by the commission were rejected by the council in 2019. Some member states—Austria, France, Italy, Spain and the United Kingdom—introduced their own digital taxes. Germany decided against it because of fears of US tariffs, for example against the German automotive industry, as a retaliatory measure. This France has already experienced: due digital tax prepayments were suspended until the end of 2020, after the US had announced punitive tariffs.

European ambition

Does fair corporate taxation inevitably lead to a trade war? A global agreement via the Organisation for Economic Co-operation and Development would certainly be desirable. Such efforts must not however prevent the EU continuing on the path of harmonisation. The economy commissioner, Paolo Gentiloni, is keen to sustain the European ambition: in the absence of agreement at OECD level in 2020, he announced a push for the taxation of digital companies in the first half of 2021. The tax is intended to be paid primarily by large US technology groups, such as Amazon and Google, but also by new market participants such as the Chinese groups Tencent and Alibaba. The French finance minister, Bruno Le Maire, has explicitly supported this initiative.

From a trade union perspective, a common European approach is essential to achieve a fair distribution of the tax burden and sustainable public finances for upward social and economic convergence. If this cannot be achieved unanimously, the instrument of enhanced co-operation among ambitious member states remains one way out of the blockage. Another would be a framework directive which defined common standards only for those countries that wanted to introduce the digital tax and the minimum tax rate domestically.

This is part of a series on Corporate Taxation in a Globalised Era supported by the Hans Böckler Stiftung