Reducing taxes on labour – personal income taxes and employers’ and employees’ social security contributions – is often seen as key to increasing employment levels. The latest crop of country-specific recommendations issued by the European Commission is a case in point. But the rationale for such a ‘tax shift’ is relatively weak. For most countries, it is likely to represent yet another much-talked-about reform with little relevance for actual employment and economic outcomes.

Higher labour costs are assumed to reduce the demand for workers. Moreover, high labour taxation may lower incentives for the unemployed and inactive to take up work as it means that the additional income to be derived from employment is too limited to fuel the motivation to work. Referring to these two reasons, the Commission (EC) has advocated a shift in taxation away from labour to the ‘least distortionary taxes’, including taxes on consumption, housing and other property, and environmental taxes (European Commission 2015: 24).

The arguments for shifting the tax burden to property and activities that harm the environment are strong, but, for various reasons, there has been little action on these fronts. The ‘tax shift’ debate thus in practice boils down to the advice to shift taxation away from labour and capital income to consumption. However, it is hard to come up with convincing grounds for this recommendation.

The method used by the EC to identify countries in need of reducing taxation is simple, but hopelessly arbitrary: countries are found to be in need of reducing their tax rates if their taxation levels happen to be significantly above the EU average (see European Commission 2015 and various country-specific recommendations).

The idea that consumption taxes are somewhat less harmful relies on empirical modelling by the OECD (2010). The OECD’s own research, however, questions the rationale for the tax shift towards consumption as it confirms that consumption taxes affect employment and hours of work in pretty much the same way as do income taxes. What can be firmly established, however, is that such a shift is regressive as it affects the lower income groups.

Where’s the link?

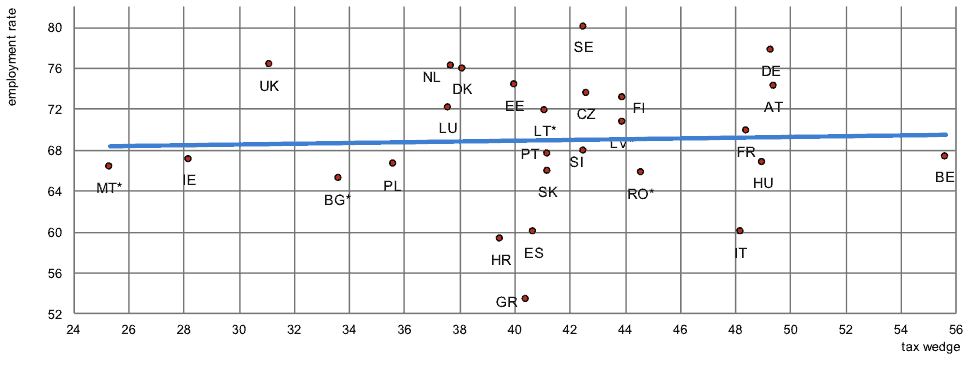

Empirically, it is difficult to separate the effect of taxes from other elements of the policy mix in individual countries. Nevertheless, a comparison of employment and tax levels in the EU, as shown in a figure taken from the ETUI’s 2016 Benchmarking Working Europe report, shows no relationship between the two. In fact, many countries with very high employment levels impose steep labour taxes. As a result, countries identified by the Commission as in need of reducing taxes on labour – i.e. Belgium, Czechia, France, Italy, Hungary, Finland and also the ‘borderline’ cases of Germany, the Netherlands, Austria, and Sweden – include these best-performing countries.

Where the crisis countries suffering from high unemployment are concerned, reducing labour costs through lowering taxation does not seem to offer any immediate respite either. As shown also by the EC’s own labour market analyses, adjustment strategies based on a reduction in labour costs have reached their limits, with countries characterised by high unemployment recording falling labour costs also.

The second rationale pointing to a possible lack of incentives to take up work is sounder.

It is plausible that high labour taxation levels may create incentive problems for the inactive or some groups of workers. They may shy away from additional employment effort due to the high taxation imposed on the additional income. Potentially affected groups include the inactive, the unemployed, second earners in a household, and low-wage earners. The EC’s analysis finds a number of such traps in individual countries (European Commission 2015: 26-27). However, even in this case, countries suffering from such traps include cases of both worst and best performance in terms of employment among the affected groups.

Finally, the ‘tax-shift argument’ has been reinterpreted in a popular version that emphasises a need to reduce social security contributions (SSC) paid by the employers in particular. Such an argument may be intuitively appealing to employers seeking to reduce any taxes that they are obliged to pay, but there is no reason why they should matter more than other components of labour taxation – in fact, they may be less relevant to incentives for workers. Empirically, there is in the EU no correlation between employer SSCs and employment levels.

Nevertheless, this thinking informed the 2015 tax shift in Belgium, reducing employer social security contributions from 33% to 25%. Ironically, despite having the highest level of taxation on labour and a unique tax mix heavily subsidizing car use, that country was a boring European average as far as its levels of employer SSC were concerned. Once again, Belgian surrealism helpfully illustrated the futility of efforts on the European level.

Figure Tax wedge on labour (average wage) and overall employment rate (20-64 years), 2014

Figure Tax wedge on labour (average wage) and overall employment rate (20-64 years), 2014

* data are available for 2013 only.

Note: Tax wedge on labour: The difference between the wage costs to the employer of a worker on an average wage, including personal income tax and compulsory social security contributions, and the amount of net income that the worker receives. Source: European Commission tax and benefits database based on OECD data (European Commission, 2015).