Facebook’s idea of issuing its own cryptocurrency has met strong criticism. Katherina Pistor has called on governments to protect citizens from the Libra, while Joe Stiglitz has said they should shut it down immediately.

Both are absolutely right. Libra is anything but a stable currency—despite Facebook’s claims.

Hayek’s currency competition

Stability is crucial for a private currency, if it wants to succeed in competition with established national currencies and the euro. This was already made clear by Friedrich Hayek in his pioneering book Denationalisation of Money, published in 1976:

It seems to me to be fairly certain that,

(a) a money generally expected to preserve its purchasing power approximately constant would be in continuous demand so long as the people were free to use it,

(b) with such a continuing demand depending on success in keeping the value of the currency constant one could trust the issuing banks to make every effort to achieve this better than would any monopolist who runs no risk by depreciating his money,

(c) the issuing institution could achieve this result by regulating the quantity of its issue, and

(d) such a regulation of the quantity of each currency would constitute the best of all practicable methods of regulating the quantity of media of exchange for all possible purposes.

The lack of stability is precisely what cryptocurrencies have been suffering from so far—above all Bitcoin, which betrays excessive volatility.

The designers of the Libra are aware of this challenge and I think they must have read Hayek. They promise to stabilise the value of their new currency in terms of a currency basket. For that purpose they want to hold reserves in the form of bank deposits and short-term government bonds, according to the currency structure of the basket. The reserves are created when investors exchange bank deposits, denominated in the established currencies, into libra.

The Libra designers therefore compare their model with the institution of a ‘currency board’, as practised in Argentina between 1991 and 2002 and still adopted in Bulgaria. A currency board is a type of central bank where the liabilities (cash and reserves of commercial banks) are in principle fully covered by liquid foreign-currency investments.

Exchange-rate risk

The problem with the Libra, however, is that it is not designed as a national, but rather a supranational, currency. The stability of the currency is therefore related to the basket and not to a specific currency.

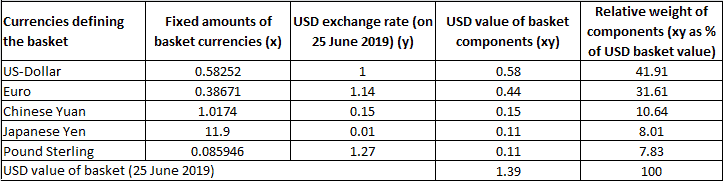

In this respect, the Libra can be compared to a basket currency such as the Special Drawing Right (SDR) created by the International Monetary Fund. The SDR is defined by absolute amounts of currencies: 0.58252 US dollars, 0.38671 euro, 1.0174 Chinese yuan, 11.9 yen and 0.085946 pounds sterling. The current exchange rate of the SDR against the euro is around 1.22 SDR/EUR. The euro’s share of the currency basket is around 32 per cent.

Currency basket of the Special Drawing Right (SDR)

Assuming that a basket structure comparable to the SDR is chosen for LIbra, the proise of value stability is not guaranteed from the point of view of national investors. If a German household were to buy 10,000 libra with 12,200 euro, it would de facto acquire foreign currencies for around 68 per cent of the amount (the residue after the 32 per cent euro share). With sometimes very strong fluctuations among the major reserve currencies, the household would take on a considerable exchange-rate risk.

Thus, investments in Libra are completely different form traditional bank deposits, denominated in the national currency. Libra is a highly speculative investment.

The smaller the share of the national currency in the Libra currency basket, the more pronounced this effect becomes. With an SDR basket share of the pound sterling of just under 8 per cent, 92 per cent of a Libra investment for a British investor would represent a foreign-currency investment. In addition, the Libra Association reserves the right to change the composition of the currency basket in the event of an economic crisis in one of the investment countries–compounding the risk.

Liquidity risk

But the exchange-rate risk is not the only one attached to the new currency. So far it is completely unclear what would happen in the event of a general loss of confidence in it.

Under normal circumstances, the exchange rate would have to correspond roughly to the book value of the reserves. Its designers believe that a ‘run’ on the Libra, with holders seeking exchange back into national currencies, could be ruled out due to the reserve coverage. This is what Hayek had in mind with the regulation of the quantity of the issue.

A sudden crisis of confidence can only be stopped reliably if every investor can expect a full repayment of Libra into the basket components. Libra can maintain its exchange rate against the national currencies on the foreign-exchange market at a constant level through intervention (buying libra against selling reserves).

The Libra reserve is however only partially to be held in ‘sight deposits’ (which are readily accessible) with banks. It is intended to invest a large amount of the reserve in government bonds. In a ‘run’ situation these assets would have to be sold very quickly, in very high amounts. The more widespread the Libra and the greater the bond holdings in the reserve, the bigger the losses on these assets would be. This liquidity risk could lead, at least temporarily, to a major devaluation of the Libra against the book value of the reserves.

The liquidity risk can be exacerbated by the fact that, by contrast with state currencies, there is no obligation to accept the Libra: it is not legal tender. Shops can refuse to accept it at any time, which would intensify any loss of confidence.

Redemption risk

What is even more important, however, is the lack of a binding redemption obligation. This substantially differs from Hayek’s proposal:

… I would announce the issue of non-interest bearing certificates or notes, and the readiness to open current cheque accounts, in terms of a unit with a distinct registered trade name such as ‘ducat’. The only legal obligation I would assume would be to redeem these notes and deposits on demand with, at the option of the holder, either 5 Swiss francs or 5 D-marks or 2 dollars per ducat.

In the event of a crisis of confidence, it is therefore unclear whether the necessary interventions would actually be made. The Libra documents explicitly state that there should be no direct contact between the users and the reserve. Rather, there should be ‘resellers’, as the only actors authorised by the association to carry out larger transactions from libra into the state currencies and vice versa.

Thus there is a fundamental distinction between a traditional bank deposit and a Libra balance. A bank deposit of 100 euro implies a legally binding commitment to redeem it in banknotes of 100 euro. A Libra deposit is merely a non-binding promise to stabilise the Libra exchange rate at approximately the book value of the reserves. A Libra deposit therefore carries a redemption risk, compared with the traditional bank deposit.

These three risks are not offset by adequate opportunities for holders to profit, even where the demand for libra is very strong. The supply is completely elastic due to the issuing mechanism: new libra can by issued without limit whenever there is a demand for the currency.

This is fundamentally different from Bitcoin. Bitcoin also has no redemption obligation. But its supply is almost completely rigid in the short term, due to the complex ‘mining’ process by which transactions are verified. So large price jumps (and windfall gains) are possible if demand rises.

Gigantic enrichment programme

The basic problem with Libra credit balances is that they are neither debt, which requires a binding promise of redemption, nor equity, which would imply some form of profit-sharing and the right to a say. For the organisers of the system, that is, of course, the big advantage. They are provided with liquidity which they can use profitably in the sense of a giant money-market fund—without having to grant depositors a share in the profits.

In the event of losses, however, the organisers cannot expect any consequences in the form of insolvency proceedings. Libra would thus become a gigantic enrichment programme for Facebook and its comrades-in-arms, at the expense of investors who do not understand the underlying mechanisms of the scheme.

The best response to Facebook’s initiative is therefore broad public education about Libra’s exchange-rate, liquidity and redemption risks. If Hayek is right, nobody would like to hold an unstable currency.

And when it comes to making international transfers quickly and cheaply, there is no need for new currencies. Adequate competition among payment service providers would suffice.

This article is a joint publication by Social Europe and IPS-Journal