As Mario Draghi’s term as president of the European Central Bank comes to an end, it’s hard to miss that he was not successful in winning the hearts of Germans. Even before the ECB’s decision to lower the deposit rate from minus 0.4 to minus 0.5 per cent on September 12th, the president of the German Savings Banks Association wrote a Wutbrief (letter of fury) to the tabloid newspaper Bild a month earlier. In his tantrum he blamed Draghi for changing the lives of millions in Germany but also in Europe—and not for the better. After the decision, Bild represented Draghi as a fanged ‘Count Draghila’, sucking German savings accounts dry.

This negative attitude is not new. A majority of the German Council of Economic Experts has criticised Draghi and the ECB’s policy as excessively expansionary for years. Back in 2014 the council anticipated risks to price stability, as well as to the stability of banks and financial markets—which never materialised.

Characteristic of the heated German debate has been its focus on the plight of the German saver. This is the most narrow perspective possible for assessing the policy of a European institution. The ECB’s mandate is not to generate adequate returns for savers but rather is laid down in article 127 of the Treaty on the Functioning of the European Union: ‘The primary objective of the European System of Central Banks … shall be to maintain price stability.’

In line with the practice of almost all other central banks, the ECB has defined ‘price stability’ not as an inflation rate of zero but as a rate ‘below but close to 2 per cent’. This reflects the insight that with a 2 per cent rate in an equilibrium situation there is more distance to the deflation threshold of recession than with a zero inflation rate.

Measured by that yardstick. the ECB under the Draghi presidency has certainly not been overly expansionary. From 2011 to 2019 the average euro area inflation rate was 1.1 per cent. As the effects of monetary policy have long lags, one also has to ask whether this target will be met in the future. But according to the Survey of Professional Forecasters, even for the longer term no risks to price stability are expected.

Positive effects

While Draghi could not fully reach his inflation target, his policy had positive effects on growth and employment. Unemployment in the eurozone, which had reached very high levels in the depths of the crisis, has receded to the pre-crash rate of 2007. In fact, with his historic, ‘whatever it takes’ speech on July 26th 2012 and the announcement of Outright Monetary Transactions that September, Draghi was able to stop a vicious circle of rising interest rates and fears of a euro break-up. With this regime change, longer-term interest rates in all member states came down and the market pressure on the weaker member states subsided. This allowed them to arrest a destructive austerity and to restart economic growth.

For Germany, with its heavy export exposure in the euro area, the positive economic performance since 2013 has been marked by a long period of strong GDP and employment growth. Thus German workers as well as German corporations have no reason to complain about Draghi’s monetary policy. Even the German taxpayer has benefitted from the extremely low interest rates for German government bonds.

An important argument of German economists for a tighter monetary policy has been the risk of an overheating, especially of the German economy. But this year German GDP growth has turned negative and is now below the eurozone average. Unfortunately, the German government is so much under the spell of the fiscal-policy ‘black zero’ that it has so far seen no reason for stabilising measures, despite the obvious signs of a recession. Thus, the additional stimulus decided upon by the ECB should be regarded as a welcome boost for the flagging German economy.

The Draghi critics were wrong in their expectation of negative effects for the financial system too. For instance, in its 2015 annual report the German Council of Economic Experts wrote that the ECB’s monetary policy was ‘leading to a build-up of risks to financial stability which could pave the way for a new financial crisis’. But under Draghi’s presidency credit growth has been moderate in all member states and most European banks are operating profitably. As for Deutsche Bank—well, one can hardly blame Draghi for its problems.

Set against that of his predecessor, Jean-Claude Trichet, Draghi’s performance looks even more impressive. In the mid-2000s Trichet did not see the financial crisis coming, although credit growth in Spain, Ireland and Greece had been excessive since the turn of the millennium. And yet in July 2008, when the global crisis was already clearly visible, Trichet raised the ECB policy rate. Indeed, in the wake of the Lehman Brothers bankruptcy on September 15th, the ECB’s refinancing rates rose still further, to 4.99 per cent, on October 8th. And in spring 2011, when the euro crisis was in full swing, Trichet once more raised interest rates—a serious mistake.

Money illusion

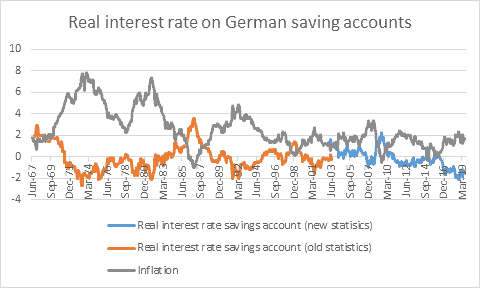

What about the implications of Draghi’s negative deposit-interest rate on the German saver? Unfortunately, the German debate suffers from the ‘money illusion’: the impact of inflation on the return of savers is completely neglected. The Bundesbank publishes historical data for the real return on traditional German savings accounts (see chart below). In the period of the Deutschmark (data are available from June 1967 until December 1998), this was -0.01per cent, mainly due to high inflation in the early 1970s and 1980s when nominal interest rates did not keep pace with inflation. In the era of Draghi (data from November 2011 until July 2019) the real return was -0.69 per cent, which is not qualitatively different.

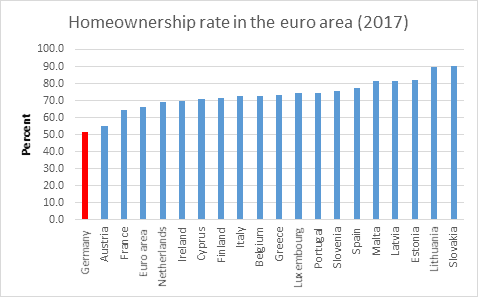

If the average German is not a Draghi fan it can be explained above all by the fact that home ownership in Germany is very low by international comparison. Only 51 per cent of German households live in their own home, the lowest ownership rate in the euro area (average 66 per cent). Thus the positive effects of low interest rates on house price were less widely felt in Germany (see barchart).

The mirror image of low home ownership is the strong preference of German savers for private retirement products—life-insurance policies—which are negatively affected by low interest rates. This unfavourable portfolio structure of German households has not fallen from heaven. Rather, it reflects the preference of German policy-makers for investments in insurance policies which are heavily subsidised by the state. Government subsidisation of home purchase by private households (Eigenheimzulage) was discontinued in 2006.

Particularly unfair

Germany’s criticism of Draghi’s policies is particularly unfair as it would have been in Germany’s hands to bring inflation in the eurozone closer to the ECB’s target. Between 2011 and 2018, unit hourly labour costs in Germany rose by an annual average of 1.8 per cent. Yet, as the fastest-growing economy, Germany should have allowed unit labour costs to rise well above the ECB’s inflation target. Only thus would it have been possible to achieve a wage trend for the whole euro area in line with it. Without appropriate support from wage policy, it is very difficult for monetary policy to achieve an inflation target.

Germany has also put the brakes on economic growth in the euro area by its near-religious fixation on the budget ‘black zero’. After an almost balanced budget in 2011 and 2012, Germany has reported a surplus in its public budgets from 2013 to the present. This was a disadvantage not only for the eurozone but also for Germany itself, given its considerable need for investment in infrastructure.

In sum, instead of criticising Draghi, Germany should be grateful to him. In July 2012 he prevented the collapse of the euro, which would otherwise have been difficult to avoid due to the lack of support from German politicians. Yet no country would have been so negatively affected by a collapse of the euro as Germany. Draghi has also succeeded in leading the economy of the eurozone out of the paralysis caused by an exaggerated austerity policy, based on the German recipe. And today Draghi’s stimulus programme is especially needed … in Germany itself.

This article is a joint publication by Social Europe and IPS-Journal