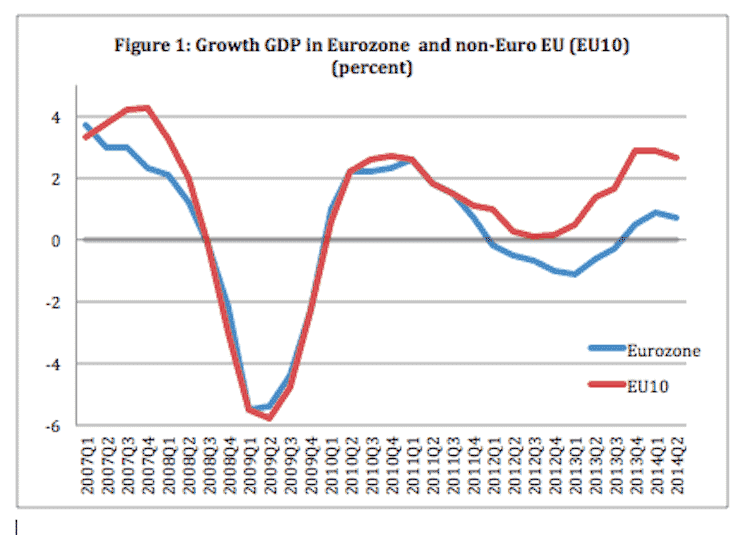

Slow growth in the Eurozone has become endemic since the start of the sovereign debt crisis in 2010. This is made very clear in Figure 1, which contrasts the growth experience of the Eurozone with the non-Eurozone EU-member countries since the start of the financial crisis in 2007. What is striking is that up to the Eurozone sovereign debt crisis of 2010 the growth experiences of the Eurozone and non-Eurozone countries in the EU were very similar. Both groups of countries saw their boom collapse and turn into a deep recession in 2008-09. Both recovered relatively quickly in 2010. Since 2011, however, the two groups of countries depart. The Eurozone experienced a new recession and since then has experienced a growth rate that on average has been 2% below the growth rate of the EU-countries that are not part of the Eurozone.

Source: Eurostat

What happened since the start of the sovereign debt crisis that has led to a systematic decline of economic growth in the Eurozone as compared to the non-Euro EU-members?

In Brussels, Frankfurt and Berlin it is popular to say that this low growth performance of the Eurozone is due to structural rigidities. In other words, the low growth of the Eurozone is a supply side problem. Make the supply more flexible (e.g. lower minimum wages, less unemployment benefits, easier firing of workers) and growth will accelerate.

This diagnosis of the Eurozone growth problem does not make sense. As is made clear from Figure 1 the Eurozone countries recovered as quickly from the recession of 2008-09 as the non-euro countries. If the problem was a structural one, it also existed in 2008-09. Yet these structural rigidities did not prevent the Eurozone countries from recovering quickly in 2010. Why then did structural rigidities from 2011 on suddenly pop-up to produce lower growth in the Eurozone than in non-euro EU-countries, while they did not play a role in 2010? Although this supply-side story does not hold water, it continues to provide the intellectual underpinnings of the Eurozone policymakers who continue to insist on structural reforms.

There is a better explanation for the Eurozone growth puzzle. This is that demand management in the Eurozone has been dramatically wrong since the start of the sovereign debt crisis. The latter led the Eurozone policymakers to impose severe austerity on the peripheral Eurozone countries and budgetary restrictions on all the others. This approach was based on a failure to recognize that the Eurozone was still in the grips of a deleveraging dynamic. After the debt explosions in the private sector during the boom years, private agents were still deleveraging. As a result of austerity, both the private and the public sector tried to deleverage at the same time. This introduced a deflationary bias in the Eurozone that led to a new recession during 2012-13, the second one since the start of the financial crisis in 2007-8.

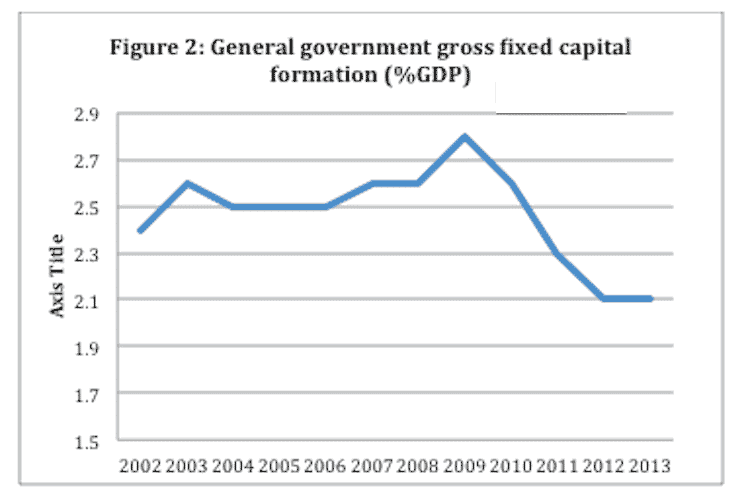

One of the most spectacular manifestations of the ill-advised austerity programs was the strong decline in public investment in the Eurozone. This is shown in Figure 2. It shows that after the sovereign debt crisis the Eurozone governments, in the name of austerity, decided to dramatically reduce public investment. How they could hope that this would promote economic growth will remain a mystery. In fact, such a decline in public investment is sure to lead to lower production possibilities in the future, i.e. to less supply in the future.

All this leads to the question of what to do today? Governments of the Eurozone, in particular in the Northern member countries now face historically low long-term interest rates. The German government, for example, can borrow at less than 1% at a maturity of 10 years. These historically low interest rates create a window of opportunities for these governments to start a major investment program. Money can be borrowed almost for free while in all these countries there are great needs to invest in the energy sector, the public transportation systems and the environment.

This is therefore the time to reverse the ill-advised decisions made since 2010 to reduce public investments. This can be done at very little cost. The country that should lead this public investment program is Germany. Public investments as a percent of GDP in Germany are among the lowest of all Eurozone countries. In 2013 public investment in German amounted to a bare 1.6% of GDP versus 2.3% in the rest of the Eurozone.

Source: Eurostat

Such a public investment program would do two things. It would stimulate aggregate demand in the short run and help to pull the Eurozone out of its lethargic state. In the long run it would help to lift the long-term growth potential in the Eurozone.

The prevailing view in many countries is that governments should not increase their debt levels lest they put a burden on future generations. The truth is that future generations inherit not only the liabilities but also the assets that have been created by the government. Future generations will not understand why these governments did not invest in productive assets that improve their welfare, while these governments could do so at historically low financing costs.

This blog was first published on Paul DeGrauwe’s Ivory Tower Blog