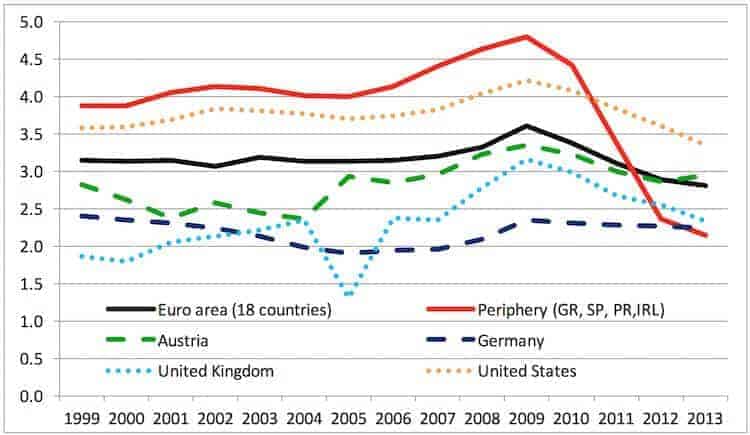

As the Euro crisis hit, European policy makers reacted with headless austerity policies and a tightening of the Stability and Growth Pact (SGP). The failure of these policies is obvious: after seven years of deep economic crisis the Euro area is on the verge of deflationary stagnation. Public investment – which should have stabilized the economies and kept up their long-term growth potential – has dramatically shrunk in the periphery (see figure). Fiscal policy has been completely disempowered, at the very moment when it was most needed.

Figure: general government gross fixed capital formation (ESA 2010) in the Euro area, the European Periphery and selected countries in per cent of GDP, 1999-2013

Source: European Commission Ameco database (November 2014); author’s calculations.

It is by now widely accepted at the EU level that a more expansionary fiscal policy is necessary, because monetary policy alone will not spark off the recovery. In his Jackson Hole speech Mario Draghi called for a more expansionary fiscal stance for the Euro area and a public investment programme. The European Council in June 2014 also saw the need to enhance growth within the existing fiscal framework. Finally, the new EU Commission has launched two initiatives substantially amplifying its predecessor’s efforts.

First, an Investment Plan for Europe, the ‘Juncker-Plan’, has been presented, i.e. a large-scale European Fund for Strategic Investments (EFSI). It is difficult to evaluate the Plan’s prospects as it is still in its very early stages. However, there are many open questions and whether it will really deliver is quite doubtful.

Second, the interpretation of the SGP has been clarified with the aim of providing more fiscal leeway for member states struggling under adverse economic conditions and/or implementing structural reforms. This may contribute to slowing down the pace of consolidation somewhat, but the clarifications are only designed to permit a slightly less restrictive fiscal stance – not to provide the required fiscal stimulus.

A Real Revival Of Fiscal Policy: The Golden Rule Of Public Investment

What might a real revival of fiscal policy designed to bring about a sustained recovery and to increase public investment look like? As I have proposed in a recent study for the Austrian Chamber of Labour, one important element could be the introduction of the golden rule of public investment. The rule is widely accepted in traditional public finance and would allow the financing of public investment by government deficits, thus promoting intergenerational fairness as well as economic growth. Public investment increases the public capital stock and creates growth for the benefit of future generations. Therefore, future generations should contribute to financing those investments via the debt service. Failure to allow for debt financing will lead to a disproportionate burden on the current generation and therefore most probably to underprovision of public investment: in fact, exactly what happened during the crisis.

In economic terms, the most plausible definition would focus on those government expenditures that provide a substantial future pay-off in terms of higher growth or avoided costs. A pragmatic version focusing on net public investment as defined in the national accounts minus military expenditures plus investment grants for the private sector could (technically) be implemented quickly. Net public investment should then be deducted from the relevant deficit measures of the SGP and the fiscal compact. This would at once protect public investment from cuts and provide leeway for investment to recover. In order to prevent a conflict between the golden rule of public investment and the goal of stabilizing public debt at below 60 per cent of GDP, an upper limit of deductible net investment spending of 1 or 1.5 per cent of GDP could be set. Over time it could be refined technically and statistically and potentially include other – more intangible types – of investment like education expenditures.

Such a golden rule of public investment could even be approximated for some time without any changes in the current institutional framework, if Commission and Council were willing to use the interpretational leeway within this very framework. However, to firmly anchor the golden rule, a change in the framework would be helpful and this could be implemented as an ‘Investment Protocol’ under the simplified revisions procedure of Art. 48 of the Lisbon Treaty. As political implementation would probably take some time, the golden rule would have to be complemented by expansionary fiscal policy to provide the urgently needed boost to the European economy in the short term.

A Complementing Short Term Fiscal Expansion (‘Silver Rule’)

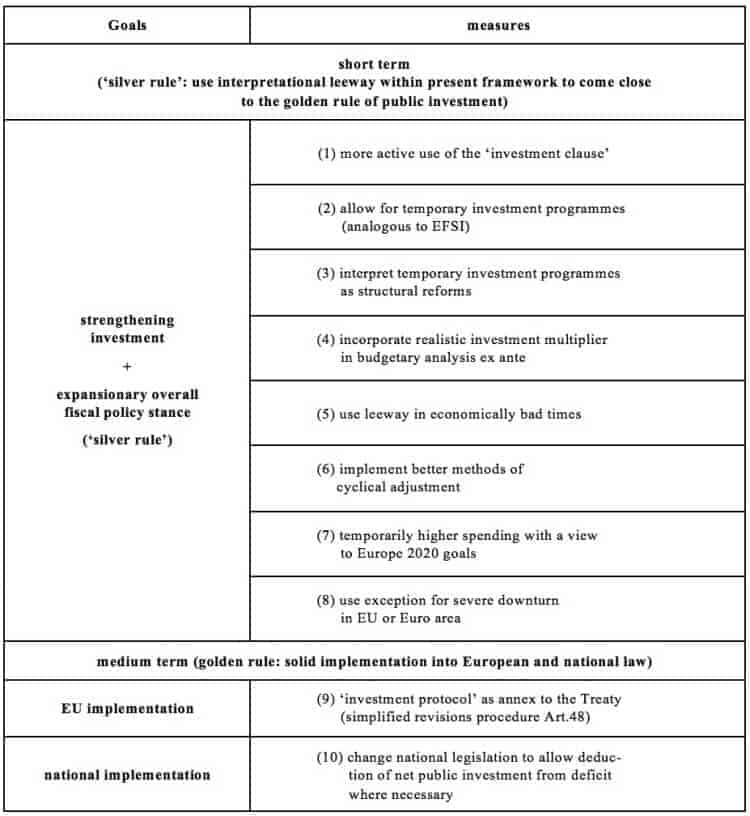

This could be done by introducing a ‘silver rule’: a short term European Investment Programme similar to the 2008 European Economic Recovery Programme during the Great Recession. Such a programme could also allow for investment needs beyond the national accounts definition to contribute to public investment in a broader sense. This could be investment in education, including child care, but it could more generally focus on spending with a view to achieving the neglected Europe 2020 goals such as social inclusion or other areas that have suffered severely from austerity over recent years. The leeway within the current institutions should be actively used to provide a substantial fiscal stimulus to the European Economy (see table).

Table: 10 ways to strengthen investment and facilitate an expansionary overall fiscal policy stance in Europe

Source: author’s compilation.

A Pragmatic Stepwise Approach To Boost Investment

The ‘silver rule’ followed in turn by the golden rule of public investment could be important elements of a strategy to reform European fiscal institutions in order to boost the economy and to strengthen and protect public investment. All it would need is the will to be a bit more consequential in using the leeway provided by the current framework in the short term. And, in the medium term, a small reform of the institutions would be necessary to enable implementation of the golden rule of public investment as a widely respected traditional guideline within public finance.

It is to be hoped that it will not once more take years of stagnation and more millions of unemployed before European policy makers draw the right conclusions and start reviving fiscal policy.