High expectations accompanied the outcome of the European Central Bank’s strategy review, presented earlier this month. Already at her first press conference in December 2019, the ECB president, Christine Lagarde, had insisted that ‘that strategic review needs to be comprehensive, needs to look at all and every issue, will turn each and every stone’.

Considering that the core of the previous strategy dated back to 1998 and betrayed considerable weaknesses at the time, the need for a thorough review was beyond doubt. But after the presentation of the results on July 8th, it is not obvious that it represents the ‘pretty strong step’ Lagarde suggested.

Incremental, not fundamental

At the heart of the matter for the ECB is the definition of the mandate of price stability. The new strategy has replaced the somewhat awkward ‘below, but close to, 2 per cent’ from the 2003 strategy review with a cleartarget of 2 per cent—with explicit reference to the symmetry (an average, not a ceiling).

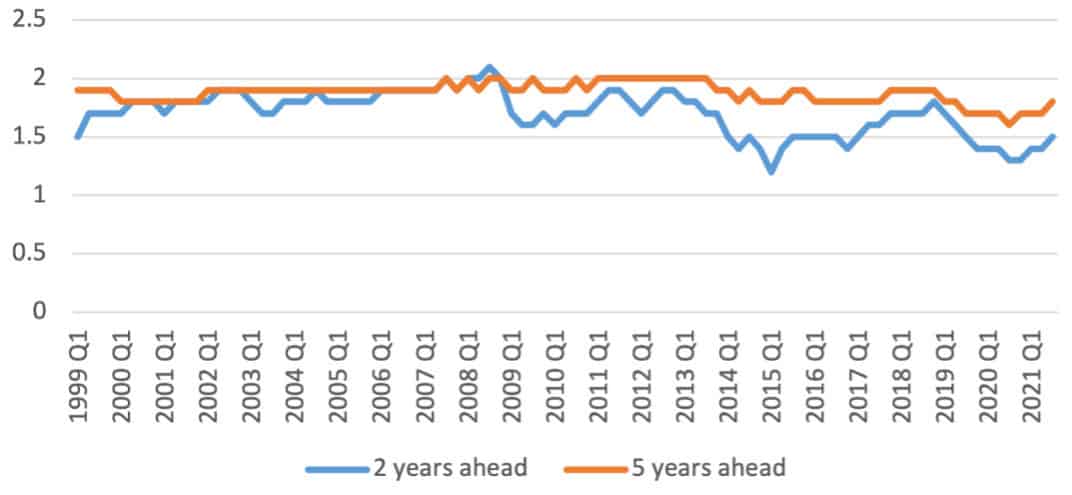

This is helpful but more an incremental than a fundamental change. Inflation forecasts by the Survey of Professional Forecasters (SPF) since 1999 indicate that from the outset the ECB’s target was regarded as a value close to 2 per cent (Figure 1). This was even true for the original target definition of ‘below 2 per cent’, replaced in 2003. Since 1999, the average of the inflation forecasts five years ahead has been 1.88 per cent, which is as close to 2 per cent on the underside as possible.

Figure 1: inflation forecasts for the euro area

The symmetry of the target is also less revolutionary than it appears. The emphasis on the ‘medium-term’, already included in the 1998 target definition, makes clear temporary deviations upwards and downwards are possible. Moreover, in March 2016 Lagarde’s predecessor, Mario Draghi, had already declared that the bank’s Governing Council understood the target symmetrically:

What I can say, however, is that our mandate is defined as reaching an inflation rate which is close to 2 per cent but below 2 per cent in the medium term. Which means that we’ll have to define the medium term in a way that, if the inflation rate was for a long time below 2 per cent, it will be above 2 per cent for some time. The key point is that the Governing Council is symmetric in the definition of the objective of price stability over the medium term.

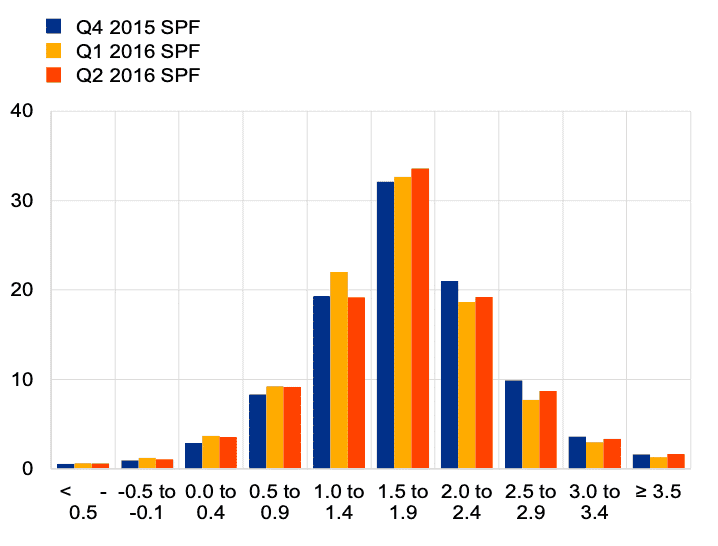

That ECB-watchers were aware of this symmetry is reflected in the probability distribution of longer-term inflation expectations, such as in the SPF forecast for the second quarter of 2016 (Figure 2).

Figure 2: aggregated probability distribution of longer-term (five years ahead) inflation expectations

Empty of content

The ECB rightly contends that a strategy should ‘provide(s) policymakers with a coherent analytical framework that maps actual or expected economic developments into policy decisions’, as well as a vehicle for public communication. That framework must thus play a prominent role. The ECB has replaced the ‘two-pillar strategy’ from 1998 with an ‘an integrated assessment of all relevant factors’—an economic analysis and a monetary and financial analysis.

Beyond rather tautological statements, the ECB elaborates the rationale in these words:

Within this framework, the economic analysis focuses on real and nominal economic developments, whereas the monetary and financial analysis examines monetary and financial indicators, with a focus on the operation of the monetary transmission mechanism and the possible risks to medium-term price stability from financial imbalances and monetary factors. The pervasive role of macro-financial linkages in economic, monetary and financial developments requires that the interdependencies across the two analyses are fully incorporated.

Thus, the analytical framework continues to be as empty of content as it was in 1998. If a strategy is to contribute to a better understanding of a central bank’s decision-making it must offer some heuristic, reducing the complexity of reality to some simple rules of thumb or cues. While monetary targeting and the Taylor rule both came close to a heuristic, they failed in practice. In contrast, inflation targeting has functioned pretty well and is now practised by many central banks in advanced and emerging-market countries.

Such a strategy reduces the complexity of monetary-policy decisions by focusing on inflation forecasts. By comparing forecasts with the inflation target, undesirable developments and the need for monetary-policy action can be identified in good time. Several independent institutions produce inflation forecasts for the euro area (Figure 3), which can render the analytical framework more objective. Due to the different forecast horizons, temporary shocks leading to temporary deviations from the target can also be identified and explained.

Figure 3: inflation forecasts for the euro area (Q3, 2021)

The ECB has missed the opportunity to develop its strategy towards explicit inflation targeting, as recommended by prominent economists (‘targeting inflation is very close to what the ECB has been doing—regardless of the rhetoric—and to what it should be doing’) from the very beginning. This is even more surprising as the bank practised implicit inflation targeting in the past: in the introductory statements to its press conferences, the detailed SPF inflation forecasts were prominently mentioned.

Public communication

The new strategy was implemented with a press conference on July 22nd. The ‘introductory statement’ was replaced by a ‘monetary policy statement’. This was supposedly ‘more narrative-based, and more concise’ but it is not obvious it has improved communication with the public.

The absent SPF inflation forecasts of 1.5 per cent for the medium-term and 1.8 per cent for the long-term would have justified the ECB’s expansionary stance, while reassuring the public that price stability was not endangered. But Lagarde insisted the Governing Council was ‘not relying on any kind of projections’. Without concrete data, however, the ‘narrative’ is less informative and also not correct: Lagarde said the bank expected inflation to ‘rise over the medium term’, when a decline is forecast in 2022 and 2023.

A further drawback is the neglect of monetary data. Although monetary growth is only very indirectly related to inflation, the 8.4 per cent growth rate of the money stock, M3, is still very high and requires attention. With the unprecedented increase in the ECB’s balance sheet, many citizens are concerned this might lead to an upsurge of inflation.

The focus of the press conference was Lagarde’s presentation of the implications of the strategy review for the forward guidance on the key ECB interest rates:

The Governing Council expects the key ECB interest rates to remain at their present or lower levels until we see inflation reaching 2 per cent well ahead of the end of our projection horizon and durably for the rest of the projection horizon, and we judge that realised progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilising at 2 per cent over the medium term. This may also imply a transitory period in which inflation is moderately above target.

After this mouthful, Lagarde had to admit: ‘I know that it’s going to take a little time to unpack it and really understand all the subtlety and the details of it.’ But if the ECB is committed to improving its communication ‘towards the wider public, which is essential for ensuring public understanding of and trust in the actions of the ECB’, why choose such cryptic language?

The bank faces a difficult balancing act. On the one hand, it has to make clear to the financial markets that no higher interest rates are to be expected in the foreseeable future. On the other, it must make clear to the citizens of Europe, who fear inflation, that there is no danger to price stability in the medium term. After the recent press conference, one could get the impression that the ECB is addressing the financial markets more than the citizens. This damages its public image—and risks turning public fear of inflation into a self-fulfilling prophecy.

This article is a joint publication by Social Europe and IPS-Journal