Economic ideas, when linked to measurement and policy-making, have power. Knowledge informs decisions and helps to justify policy in public. In the current moment this rationalist conception of policy needs defending against ‘post-truth’ politics.

But confronting outright irrationality and ignorance is the easy part. What about the role that economics itself plays in upholding the existing order of things, warts and all? From their inception in the 18th century economic ideas and statistics have been deeply political. And it is not just the big ideas—such as the ‘freedom to choose’ and the ‘market knows best’—that matter. Seemingly innocuous concepts may have significant effects in constraining policy and shaping social and economic reality. They buttress normalised denial. The notion of the ‘output gap’, a concept and statistical measure buried in the heart of European economic policy-making, is one such variable.

The basic idea behind ‘output gaps’ is clear enough. Monetary and fiscal policy must be benchmarked against something. It is not enough to say that fiscal policy is expansive or monetary policy is tight. What we need to know is the state of the economy on which policy is acting. In response to a recession a fiscal boost will be appropriate. But how far should it go? The answer depends on how depressed the economy is—how far its current cyclical level is from its structural potential. Conversely, in response to a boom one would expect a tightening of policy, all the more so because a boom will tend to improve the fiscal position by generating extra tax revenue. But, again, by how much?

In making such judgements, our assessment depends on the gap between current output and a figure that is not directly observable—potential output. The question is how to estimate the benchmark of potential output.

Cottage industry

Since the 1960s, when the Yale economist ‘Art’ Okun first formulated the basic idea, a cottage industry has grown up calculating output gaps. The International Monetary Fund, the Organisation for Economic Co-operation and Development and the European Union publish estimates for all the major advanced economies.

Nor are these merely innocuous statistical exercises. Estimates of the output gap are at the heart of the so-called Greenbook forecasts provided to the board of governors of the US Federal Reserve system. In the EU’s budgetary framework, ‘output gaps’ serve as the basis for estimating the ‘structural budget balances’, which define the fiscal objectives for each eurozone member. Countries that are below their potential are given more fiscal leeway. The reverse applies to those with ‘positive’ output gaps. According to the Fiscal Compact, operative since 2013, structural deficits should be reduced at the rate of 0.5 per cent per annum.

But how is potential output calculated? Not only is it a hypothetical figure but, if the notion of potential is taken seriously, it also involves guesses about the future. The question has worried experts from the start. In the European Commission’s framework, potential output is notionally defined as the output at which capital and labour are employed at ‘non-inflationary levels’. Price stability is thus made the basic parameter determining sustainable output and output growth.

Figures for the capital stock are derived from a database know as AMECO. They are a relatively fixed element in the calculation. What really drives the estimates are figures for employment and productivity growth. To estimate their long-run sustainable growth paths, the commission economists employ a statistical technique known as a Kalman Filter. In layperson’s terms this is roughly equivalent to a rolling average of past performance. This means that potential output is derived from its own historical trends, continuously updated with the latest available information.

Extrapolating from past data means that potential output estimates are anchored in historical experience. But it also means that estimates of potential are not, in fact, independent of the record of actual production. When combined with stringent fiscal rules, backward-looking estimates of potential output can have truly perverse effects.

If an economy is growing rapidly, as the eurozone was before 2008, potential output will be revised upwards. As economies like Ireland and Spain were booming, the estimates of their potential output became more generous, making their actual growth appear less excessive. That in turn meant that their fiscal stance was judged to be adequately tight. Expertise helped to reinforce excessive optimism.

Since 2008 we have confronted the reverse effect. Due to the working of the econometrics the prolonged recession in the eurozone has depressed the commission’s estimates of potential output. This has the effect of narrowing the gap between actual and estimated potential output. As expectations were diminished and lower growth and higher unemployment were redefined as normal, the case for corrective fiscal policy stimulus was weakened. The apparent fiscal room for manoeuvre diminished.

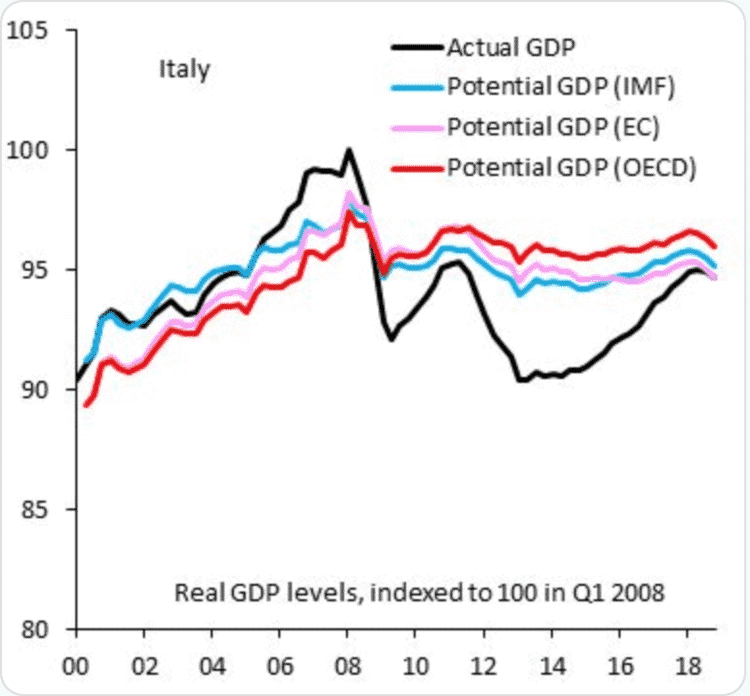

In the Italian case the effect was dramatic. In 2018, ten years on from the onset of the crisis, with high unemployment and low growth having become the norm, Italy’s potential output estimates were revised downwards by between 15 and 20 per cent—so even a modest amount of economic growth was enough to push Italy above its potential output limit to record a positive output gap. With unemployment still close to 11 per cent, its economy was declared to be overheating. It would be an absurdity if the government in Rome had not been embroiled in a knife-edge battle with Brussels over its budget, an argument in which the structural budget balance played a key role.

Of course Italy has more problems than simply its budget deficit. What is really pressing is its debt, the inheritance of budgetary indiscipline in the 1980s and 1990s. Its education system fails too many of its young people. Its labour markets are inflexible and its public administration sclerotic. No doubt the pressure of globalisation on Italy’s export-orientated manufacturing economy is becoming more severe by the year. But it is implausible to argue that all those factors suddenly intensified so dramatically as to explain the slump in growth after 2008. A significant part of Italy’s slowdown is accounted for not by a levelling out of potential growth but by demand failure.

Terrible politics

Bad estimates of output gaps don’t just make for bad economic policy. They make for terrible politics too. If one wanted to write a script to bolster the claims of anti-system politics in Europe, it would look like the policy position of the commission. Right-wing nationalist politicians promise a bold new future. Many of those promises are unrealistic and irresponsible; it is right to denounce them as such. But to adhere to the absurd claim that Italy in the spring of 2019 is broadly in the same cyclical position relative to its national potential as Germany—around 0.3-1 per cent above potential—positively invites such a wilful response.

If centrists want to win the political argument they must offer their own constructive vision of the future. A technocratic sliding scale, which limits the notion of a member state’s potential to mechanical projection of the last dismal decade, is not realistic but fatalistic.

As the sociologist Harold Garfinkel once remarked, there are usually good organisational and political reasons for bad data. The EU is a highly complex political body. Since 1999 the so-called Output Gap Working Group of the Economic Policy Committee of the European Council has developed formalised working procedures. The basic criteria of the model it has developed, which underpins the commission’s published estimates, are transparency and assurance of equal treatment of members. Politics dictates that it must be a one-size-fits-all approach.

This is bound to work for some states better than for others—which is where the unspoken third requirement comes in. Whatever formula is devised must gain the approval of the most conservative member states. The output-gap estimates, in short, are politics pursued by the technical means of economics.

Who then can shake the commission out of its intellectual reproduction of a regime of economic stagnation? Criticism from the broader public is important, but it is too easily ignored by those on the inside of the apparatus. That is why the social-media campaign ‘Against nonsense output gaps’ mounted by Robin Brooks, chief economist of the Institute of International Finance, is noteworthy.

The IIF is the lobby group of the financial industry. It represented the banks in the negotiations over Basel III regulation and the creditors in the Greek debt talks of 2011-12. These are no outsiders. And Brooks seeks to mobilise an even more important expert constituency, the IMF.

The fund might not seem an obvious partner to call on in critiquing an excessively restrictive fiscal mechanism. From the first Greek bailout of May 2010, it was deeply involved in the botched handling of the eurozone crisis. But its retrospective reviews have been admirably frank in their criticism of its entanglement with the disastrous policy of ‘extend and pretend’, particularly in Greece. Several IMF economists came forward to criticise the deal in Ireland. As chief economist Olivier Blanchard demolished the intellectual rationale for austerity. When it comes to the present state of the eurozone, however, the fund relapses into whitewash.

Extraordinary claim

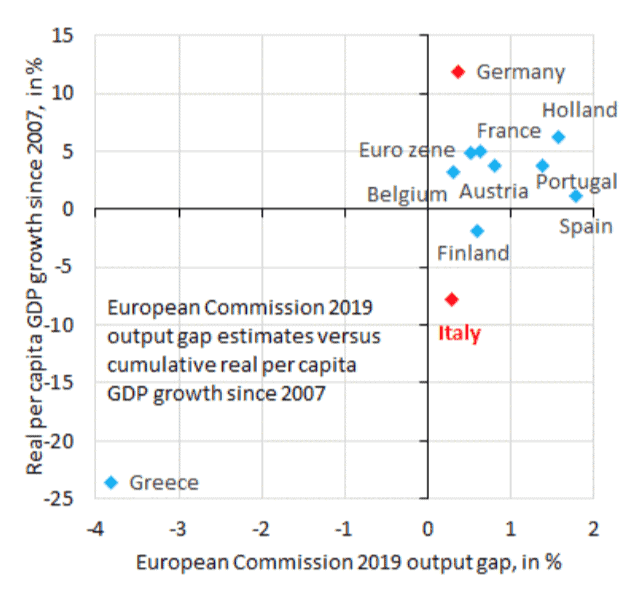

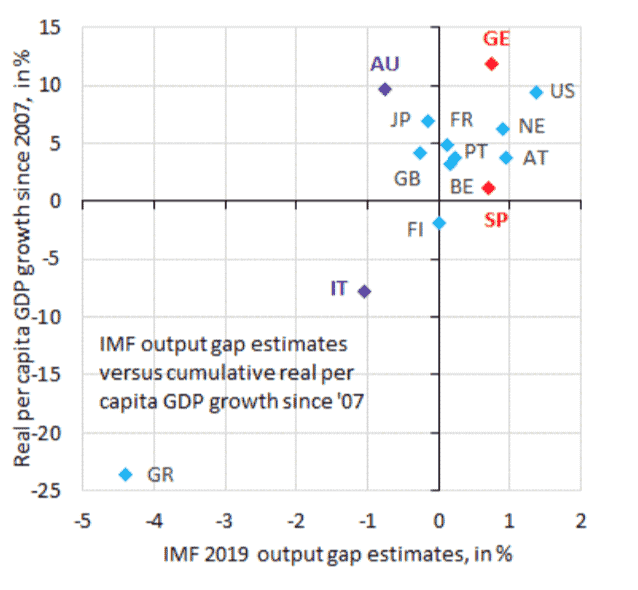

In the spring of 2019, the IMF published its assessment of the state of the major advanced economies. Inevitably this included estimates of the output gap. Unlike the commission the fund assesses Italy as below its potential, but only by 1 per cent. This is an extraordinary claim. According to the IMF’s own data, in per capita terms Italy’s economy has shrunk by 8 per cent since 2007. At the same time Germany’s has grown by 12 per cent and that of the US by 10 per cent—yet in cyclical terms all three are judged to be within 1-1.4 per cent of their potential output.

Such misleading statistics obscure what ought to be at the centre of policy debate. If we accept the output-gap estimates at face value, then all attention needs to focus on the fact that Italy’s growth potential has collapsed. It has suffered an exceptionally severe structural crisis and reviving investment has to be the priority. If the potential-output figure is wrong, however, then Italy is, in fact, well below trend and the IMF should be calling on the eurozone to orchestrate a significant counter-cyclical fiscal stimulus.

What is unconscionable is to produce data which suggest that the appropriate fiscal stance for Italy and Germany should right now be broadly similar. This is to normalise an economic-policy disaster.

Of course, Italy’s high debt means that pursuing a more expansionary policy is hedged with risks. But that is an issue which must be addressed at a European level. What is undeniable is that there is no good solution, fiscally or politically, unless Italy’s economic growth revives.

Abandoning the bromide of bad data will not by itself produce a solution. But without acknowledging and accurately accounting for the miscarriage of economic policy in Europe since 2008, we cannot move forward in political or policy terms.

All graphs sourced from @RobinBrooksIIF. This article is a joint publication by Social Europe and IPS-Journal