The Franco-German summit in Deauville in October 2010 established that eurozone member states’ management of the risk of public and private debt would not benefit, in the first instance, from external assistance from the institutions of the European Union. Before securing support from outside, the state in difficulty should involve the private sector in losses.

This decision—formally intended to avoid the contagion of the global financial crisis from one member state to another—left no space for financial operators to bet on a eurozone based on risk-sharing. Since then, the mantra of risk reduction in the euro area has therefore passed through policy interventions which have segregated risks within individual countries.

Strongly interrelated

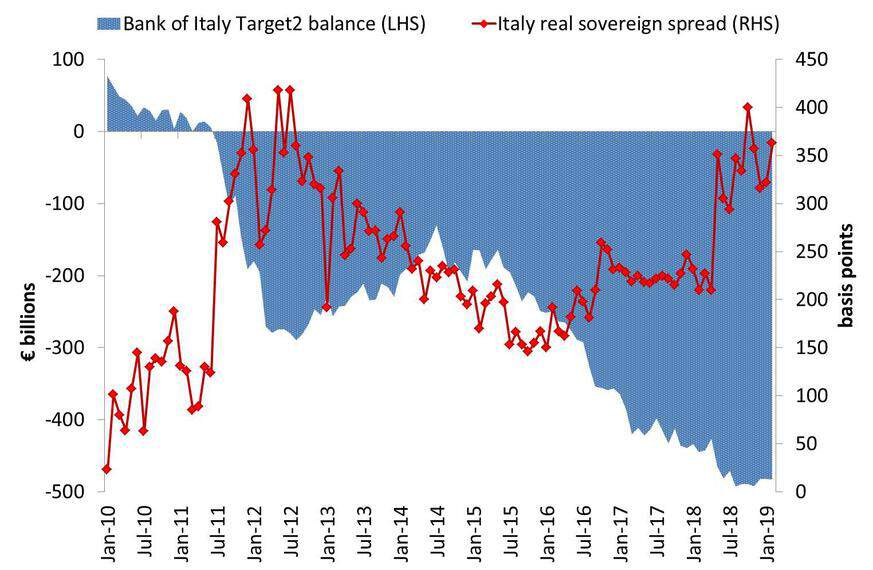

Real sovereign spreads and Target2 balances are the two quantities which best capture this phenomenon and they are strongly interrelated.

The real spread is the excess yield, net of inflation, of a eurozone member’s government bonds, compared with the German Bund. Risk comparison between two sovereign debts must rely on real yields because inflation erodes the value of a debt over time.

Target2 is the system by which cross-border payments between eurozone countries are settled through the accounts of the respective national central banks (NCBs). The system accounts for payments in a balance, which in the aggregate measures rather well the size and direction of capital flows.

Clear link

On a financial level, the link between real spreads and Target2 balances is clear. For example, if a German bank disposes of a BTP (Buono del Tesoro Poliennale—multi-year treasury bond) by selling it to an Italian counterpart, the settlement of this transaction will result in an increase in the Target2 balance of the Bundesbank and a simultaneous reduction of that of the Bank of Italy; at the same time, the sale of the BTP will create upward pressure on the Italian spread. Similarly, if an Italian family buys a car from a German company, the Target2 balance of the Bank of Italy will worsen, that of the Bundesbank will improve and meanwhile the greater demand for cars will help invigorate inflation in Germany and increase the spread in real terms.

It is therefore no coincidence that, since the beginning of the crisis, Italy’s real spreads and Target2 balances have moved in unison, albeit in opposite directions. While the spread has risen, the Target2 balance has fallen.

The European Central Bank’s ‘quantitative easing’ has somewhat dampened this dynamic—the bond-buying programme has generated downward pressure on spreads. But at the same time some of its technical features—such as the purchases having been almost entirely realised by NCBs—have favoured risk segregation to the detriment of peripheral countries, pushing the Target2 liabilities of their central banks to new record highs.

Taking the QE effect into account, I have estimated that, on average, €100 billion more of Target2 deficit for the Bank of Italy is associated with an increase in the real spread between Italian and German treasuries of over 50 basis points.

Hedging the Bundesbank

Nationalisation of public debts and capital flight from the periphery fuelled this perverse link—up to the point that nowadays even politics has become very attentive to these issues. In early June, the Bundestag discussed motions from two parties, the Free Democratic Party and Alternative für Deutschland, to guarantee the Bundesbank’s huge Target2 credit (€934 billion) in the event of a debtor country leaving the euro area. In particular, the FDP proposed that in such a scenario any Target2 liabilities of the leaving country should be previously converted into euro-denominated government bonds, so as to hedge the Bundesbank against any possible loss, including that associated with the redenomination risk.

The Bundesbank has observed that this proposal is theoretically viable, but difficult to implement, and has also recalled that Target2 ensures that every euro has the same value in each member state. An unusually dovish position—perhaps because the president of the German central bank, Jens Weidmann, was at that time in the running for the ECB presidency. In 2012 he himself recommended a hard collateralisation of Target2 liabilities, even with the gold reserves of the NCBs.

Of similar content are several other proposals originating in the core countries, such as the introduction of a floor to Target2 liabilities or a periodic settlement of these positions between the central banks participating in the euro system. In short, the centre of the euro area is thinking of how to protect itself from the possible non-cooperative exit of a debtor country such as Italy (€486 billion Target2 liability).

Segregation of risks

Not a word, instead, about whether the huge Target2 passive balances reflect the segregation of risks within the periphery or whether the Bundesbank’s giant claim is fed by a trade surplus pumped up by unfair competition with European partners, advantaged by financing manufacturing production at lower interest rates.

In addition, supporters of the above proposals do not seem to care that any limitation on Target2 would legally establish a different value of the euro in each member state.

In practice it is already so. Since the eurozone sovereign-debt crisis, Italy’s real spread has always remained of the order of 340-400 basis points. How can one compete on equal terms if the cost of money is different while the currency is the same?

Pathological set-up

This pathological set-up must end soon. As for Target2, the establishment of interest expenses for creditor countries and interest receivables for debtor countries (rather as assumed by Keynes for the operation of his international bancor) would help to normalise balances.

With regard to real spreads, the only way to make them vanishing is to move gradually to sovereign risk-sharing in the medium-long term, with market-based reforms of the (few) existing supranational bodies of the monetary union such as the European Stability Mechanism. In the short term this entails abandoning the ECB’s capital-key rule determining the QE purchases (based on relative sizes of national economies and populations), in favour of determination by the real spread or the ratio of public debt to gross domestic product.

If, instead, the eurozone continues to segregate risk, it will remain subject to the risk of break-up. Any limit to Target2 can only speed a similar drift.