It’s a well-established fact that the eurozone as a monetary union is a weird animal. Among the main reasons that surely stands out is its one-size-fits-all monetary policy that does not fail to be continually targeted by criticism from economists, politicians and other stakeholders in the various member countries.

The ECB’s monetary policy interventions share the mandate constraints of this important institution, which can be summarized in two points:

- The primary objective to maintain price stability with an inflation target lower but close to 2%

- The statutory ban on monetary financing

Without prejudice to the objective of price stability, the ECB can also support the general economic policies of the euro area including those aimed at pursuing full employment and balanced GDP growth.

Put simply, the euro system can contribute to the achievement of other objectives but price stability must be its first and foremost concern. Such exclusivity of mission is rooted in the ideological attachment to the low inflation favored (obsessively) by the Bundesbank, of which the ECB represents de facto the twenty-first century heir.

Yet, having an inflation target for the eurozone as a whole is equivalent to saying that such a target has to be pursued on average across member countries, thus admitting more or less significant inflation differentials between these countries despite their common belonging to the monetary union.

And – as it is well-known – inflation differentials matter especially when they cannot be rebalanced by exchange rate adjustments. We had a taste of this in the early 2000s when Germany hit all records as top low inflation country in the euro area and cashed in on the related competitive advantage. This has generously rewarded Germany’s vocation to pursuing mercantilism – a policy also supported by the vendor financing strategy wisely implemented by its domestic banks.

Competitiveness gaps among Eurozone members

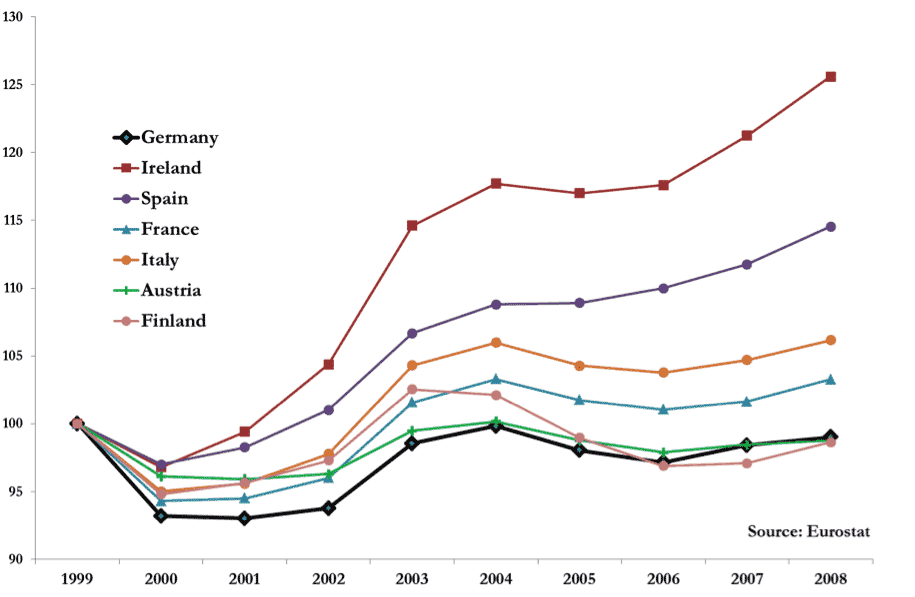

A look at BIS data (see below) on the Real Effective Exchange Rates (REER) helps to capture the competitiveness gaps induced by inflation differentials before the onset of the crisis. Figure 1 reports the REER for selected eurozone countries over the period 1999-2008 showing that – apart from a somehow correlated pattern (especially up to 2004) – a deterioration in competitiveness occurred in those years for most countries, with the noticeable exception of Germany and its allied states (Finland and Austria), which indeed enjoyed overall a depreciation of their real effective exchange rates.

Figure 1 – Real Effective Exchange Rates for selected Eurozone countries: 1999-2000 (1999=100)

The exclusive focus of monetary policy on the inflation target for the eurozone as a whole and thus (it is worth repeating) in average terms across member countries has important implications also in terms of real interest rates. The British economist Alan Walters had predicted it when he advised Margaret Thatcher not to join the Exchange Rate Mechanism (the preparatory phase for the launch of the single European currency), highlighting the inherent instability of a fixed exchange rate system. In the absence of rebalancing mechanisms replacing bilateral exchange rate adjustments, such a system is vulnerable to large gaps between participating countries and to dynamics that amplify economic cycles at the national level.

The Walters prophecy was fulfilled: before the crisis Germany was living with high real interest rates owing to low inflation, while elsewhere (e.g. Spain) rapid price growth had pushed real rates into negative territory. Consequently, investment propensity had fallen in Germany (even though this did not materially affect an economy which traditionally is more mercantilist-driven than internal demand-driven) and, conversely, low real rates have further heated high-inflation economies fueling the investment boom and the real estate bubble.

The advent of the crisis progressively reversed these trends with an associated update of their pro-cyclical implications: Germany is now experiencing negative interest rates which are a valuable support for its economic growth, while in other countries (e.g. Italy) the mix of low inflation and a high real interest rates environment hinders economic recovery. In addition, further variables have intervened to feed divergences among eurozone countries; among these stand out the breakdown of the single interest rate curve for euro area sovereign issuers (meaning different costs of debt servicing for countries of the same currency area) and the anomaly of the German Bund as a safe asset of the entire monetary union.

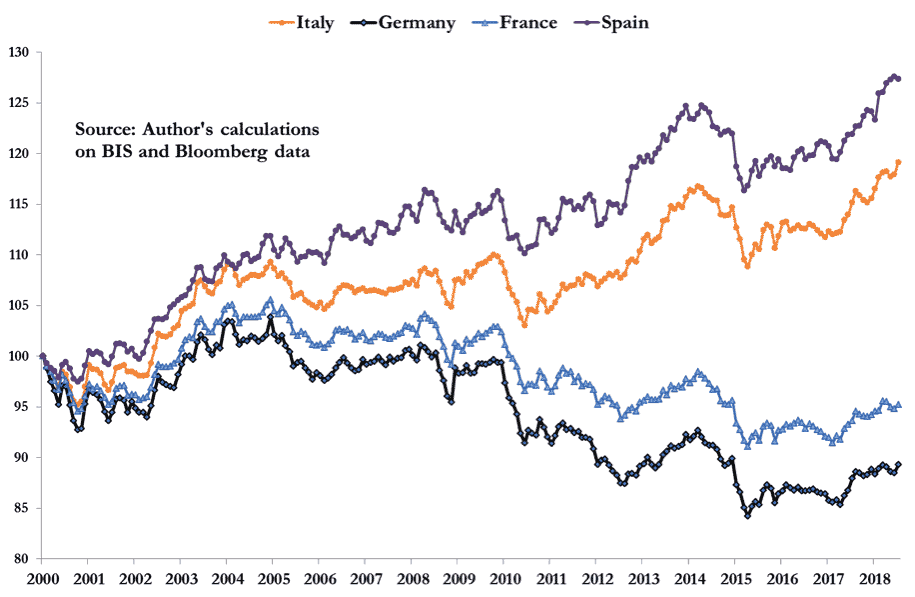

Just to take into account the combined effect of these two disaggregating factors (inflation differentials and sovereign yield spreads) on the relative competitiveness of eurozone members, I developed a new indicator – which I called Financial Real Effective Exchange Rate or F-REER – that corrects the REER by taking spreads into account. The underlying rationale is simple: sovereign yield spreads necessarily translate into different funding costs for businesses resident in the various member states, thus causing undue competitive advantages for the economy that can rely on lower interest rates.

Figure 2 compares the F-REER for selected Eurozone countries showing how our monetary union has never been united and how, in terms of commercial strength, Germany is the undisputed winner.

Figure 2 – Financial Real Effective Exchange Rates for selected Eurozone countries: 2000-2018 (2000=100)

The Eurozone inflation paradox and the riskiness of Treasuries

In the main currency areas, the central bank can finance government spending (so-called deficit monetization) through more or less direct interventions. Furthermore, the monetary authority typically has a dual mandate that includes – with equal validity – price stability and full employment. This produces a double influence on prices, also due to the retroactive effects of decisions impacting on wages. For these reasons, in currency areas such as the US, inflation is an endogenous risk for government bonds and it is correct to examine their yields in nominal terms: FED backing implies that for US Treasuries the insolvency risk is absolutely marginal compared to the unknown represented by future inflation.

In the eurozone, however, it does not work that way. The pursuit of an average inflation target in the sense seen above and the prohibition on monetary financing paradoxically imply that the ECB’s effective capacity to control the inflationary dynamics of individual member countries is minimal; in practice, these dynamics end up responding mainly to other impulses such as the level of wages and energy prices which are in turn conditioned by idiosyncratic national factors.

An important consequence of this set-up is that for eurozone government bonds inflation is an exogenous source of risk. On the other hand, the risk of outright default arises since there is no lender of last resort for national governments and still today the hallmarks of EMU governance are a strong aversion towards risk sharing and a bias in favour of fiscal orthodoxy. It follows that the comparison of sovereign yields in real terms (i.e. after adjusting for inflation differentials) allows a more correct assessment of the different insolvency risk of the various member states.

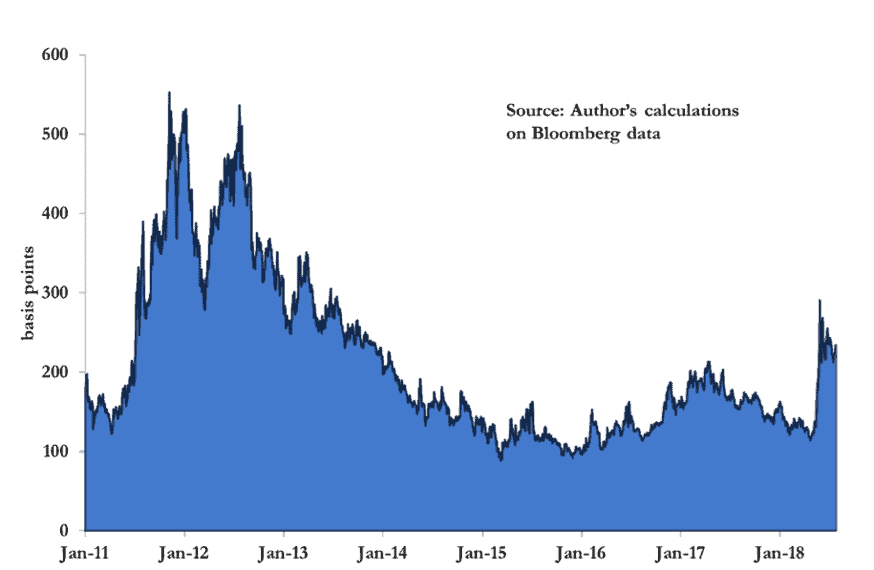

A similar analysis is of particular interest for Italy, also considering that it is the only country in the euro periphery that has not benefited from targeted assistance programs from European institutions. In recent years people have got used to consider the nominal BTP-Bund spread as the main indicator of the risk of Italy (see Figure 3).

Figure 3 – 10-year BTP-Bund spread in nominal terms: January 2011- August 2018

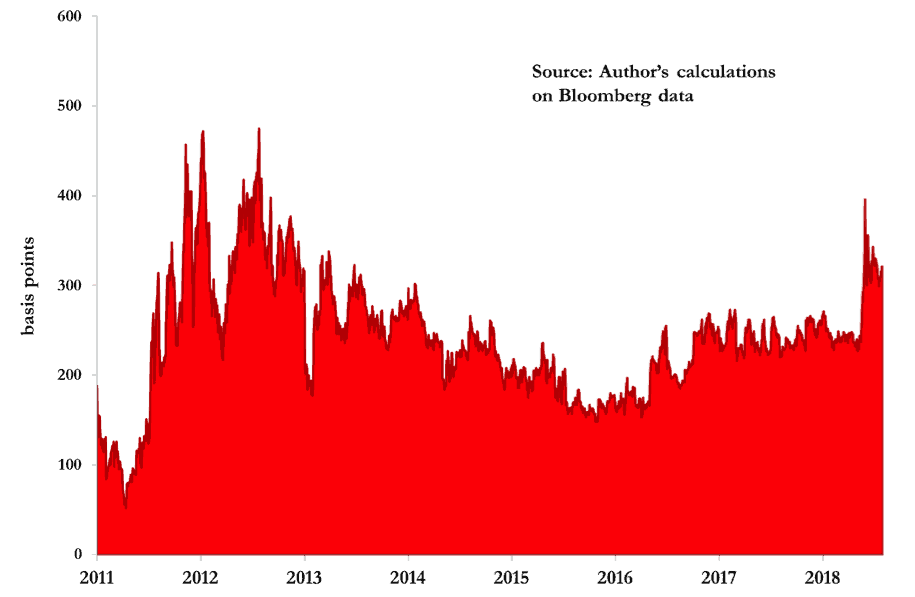

Looking at this indicator, one gets the impression that the risk associated with Italy significantly reduced in the period 2015-2017 in conjunction with Quantitative Easing (QE) and then increased again, especially in recent months. But moving the analysis to the real spread, i.e. adjusted for the inflation differential between Italy and Germany, a different dynamic emerges as shown in Figure 4.

Figure 4 – 10-year BTP-Bund spread in real terms: January 2011- August 2018

Apart from a bit of volatility, the real sovereign spread for Italy today travels on very similar values to those of seven years ago. At that time, this indicator was around 350 bps on average, just 40 above the average value over the last 4 months.

This suggests that Italy’s risk profile has not improved significantly over time: in practice it has been never below 150 bps since mid-2011 and permanently above 200 from the end of 2016. Nor should such evidence cause surprise since nothing has been done to reduce risks at the EU level apart from forcing ‘rogue’ countries to implement harsh internal reforms (see also here).

The same QE should be counted among the non-decisive measures for increasing the eurozone’s robustness and resilience. This huge purchase program provides for a minimal risk sharing on purchased bonds (indeed each national central bank is the main buyer of the debt issued by its own government) and allocates purchases according to the capital key criterion that has nothing to do with the inflationary conditions of the various members. Germany is the first beneficiary of bond purchases despite an almost non-existent deflation, while Greece is out of the program despite an epochal price slump.

Similarly, other measures adopted by the Eurozone institutions – such as the establishment of supra-national bailout funds or the recent initiative on European Safe Bonds or Esbies – insist on rejecting risk sharing and on making any form of external support conditional upon demanding commitments from national governments. Risks remain and the anti-crisis interventions of the euro-bureaucracy have mainly played for time without confronting the real problems.

The result is that today the situation appears more unstable than a few years ago given the more than doubled energy price, the biased nature of the euro-bureaucracy debate (focused more on the management of potential leavers than on risk sharing), and the forthcoming ending of QE.

No scope for risk sharing and redenomination risk

This unstable scenario raises centrifugal impetuses that put a strain on the robustness of the eurozone, as emerges also from electoral results of recent years in several member states.

Accordingly, markets began to price the so-called redenomination risk, that is the risk that euro-denominated government bonds could be converted into the newly minted national currency of a hypothetical secessionist country. It happened last year in France during the election campaign and, in recent months, in Italy in response to the political uncertainty related to the new government coalition, with spin-overs in other peripheral countries.

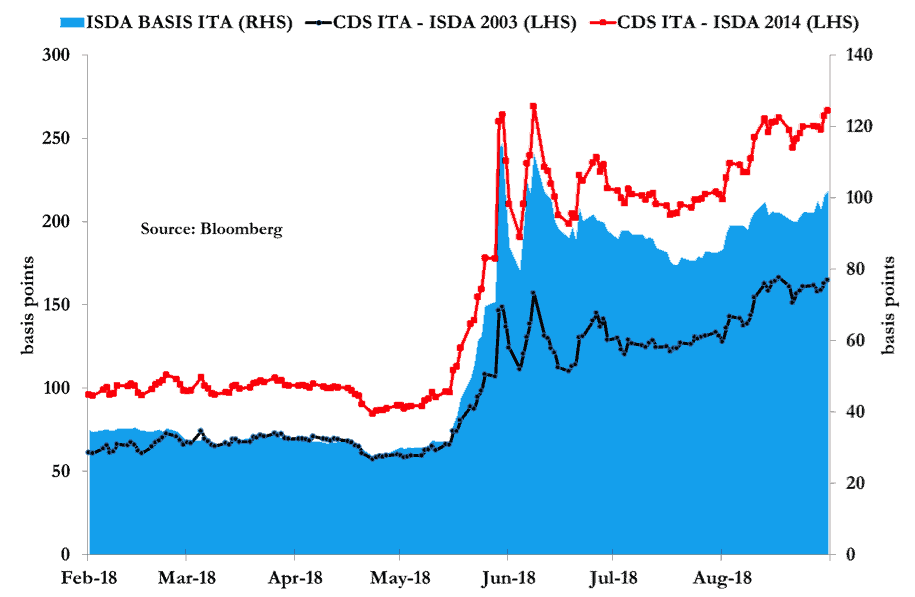

The main indicator of the redenomination risk is the ISDA basis that is defined as the extra premium on sovereign CDS contract under the 2014 ISDA standard with respect to the same contract under the (previous) 2003 ISDA standard. Such a basis is due to the fact that only the 2014 standard includes debt redenomination – provided that it entails a loss for bond-holders – among the events triggering a restructuring and, consequently, the protection offered by the CDS.

Figure 5 highlights a significant spike of the redenomination risk for Italy since mid-May. This has extended also to Spain and Portugal.

Figure 5 – CDS ISDA 2014, CDS ISDA 2003 and ISDA Basis for Italy

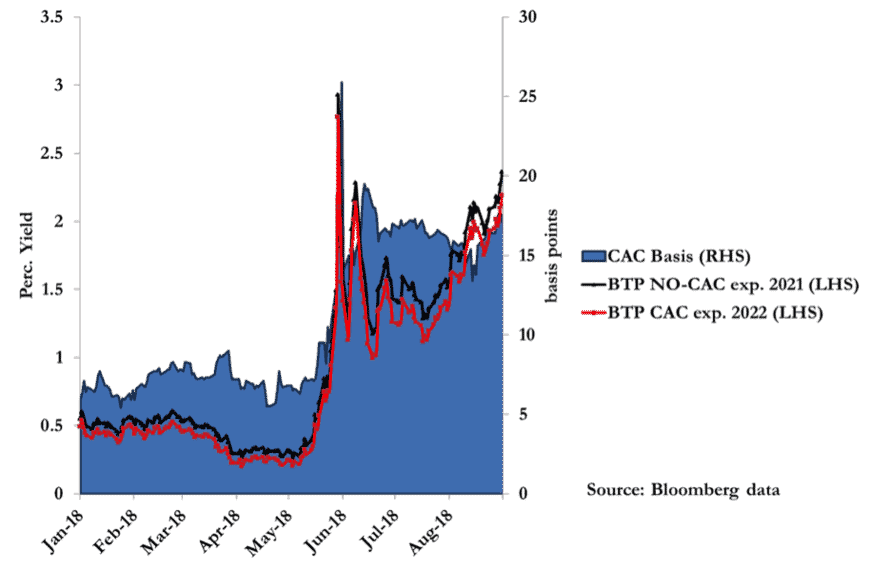

Similar dynamics are also exhibited, on a smaller scale, by the so-called CAC-basis (see Figure 6). Model-CACs (or Collective Action Clauses) were introduced in eurozone govies from January 2013 to make restructurings easier after the Greek default of March 2012. The analysis of the market of Italian govies reveals that CAC-bonds are a safer asset than their non-CAC equivalents if investors’ main concern is redenomination: indeed, given current quora, a minority of CAC-bondholders may hinder such a modification which instead remains an option available on non-CAC securities. Consistently, the CAC-basis (which measures the implied yield spread between non-CAC and CAC bonds) sharply widens in response to an enlarged perception of the redenomination outcome.

Figure 6 – CAC Basis for a pair of comparable Italian government bonds of similar maturity

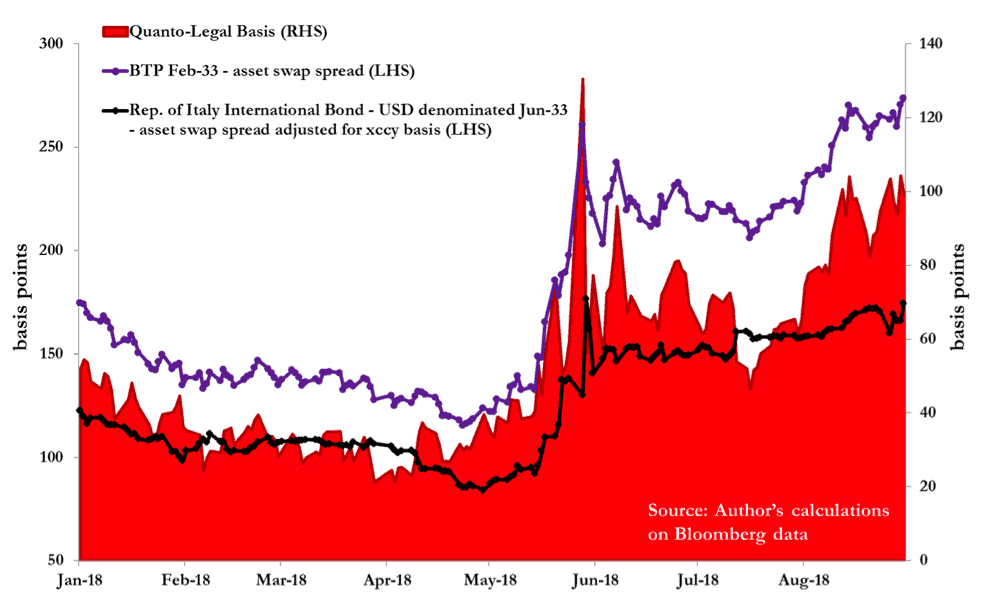

A third indicator of the redenomination risk perceived by financial markets is the Quanto spread, that is the yield spread between USD-denominated and Euro-denominated bonds of the same sovereign issuer. Often, the Quanto spread gets combined with the so-called Legal Basis, meant as the yield difference between local law and foreign law bonds: this basis widens in pressure times as Lex Monetae cannot be applied to foreign law bonds which consequently are protected against the redenomination risk. In order to properly compare bonds denominated in different currencies (and, thus, priced with respect to different risk-free curves) a standard metric is their asset swap spread, adjusted for the cross-currency basis.

Figure 7 below displays the joint value of the Quanto Spread and of the Legal Basis for a pair of comparable Italian government bonds expiring in 2033: a euro-denominated Italian-Law BTP and a USD-denominated bond issued by the Republic of Italy under an international issuance program and subject to New York law. Clearly, over the last months the bigger uncertainty surrounding the future of Italy as a member of the euro area has pushed investors to short the first security and go long on the second.

Figure 7 – Quanto Spread and Legal Basis for a pair of Italian government bonds expiring in 2033

The increased market sensitivity testified by the above indicators reflects investors’ awareness of the risk segregation which characterises the European monetary union. Rather than persisting with the argument about risk reduction and fiscal discipline at the national level, it would be appropriate to take advantage of the ongoing debate on eurozone reform to move towards a genuine risk-sharing approach.

Hence the importance of completing the banking union with the European deposit insurance scheme and opening to feasible proposals for the mutualisation of sovereign risks, such as the one I developed with Dosi, Roventini and Violi. This provides for an ESM supranational guarantee on public debts of all member states: such a guarantee, paid at fair market conditions and conditional upon a set of constraints to discourage moral hazard, would be a balanced solution to restore credibility to a battered periphery on which the future of the entire eurozone depends.