With up to €60 bn of debt a month being bought for the next 19 months, the ECB’s programme of quantitative easing (QE) is massive. But its programme suffers from three major shortcomings (see below). These shortcomings imply that the ECB’s QE programme, even if it does represent a major leap, needs serious redesigning. It must ensure that printing additional money is closely linked with a European investment plan.

The ECB has allowed the genie of deflation to escape

The first shortcoming is that the ECB’s decision to engage in a major QE programme comes way too late and after the facts. It is not just that the bank has allowed a continuous slide in both core as well as headline inflation, with the latter even turning negative in December 2014. The problem is also that medium (5-year) and even long-term (10-year) inflationary expectations are falling and are now around respectively 0.5% and 1% only.

By allowing these trends to materialise, the ECB is playing with fire. If employers and workers internalize low inflation and falling inflationary expectations when setting prices and wages, then we have a self-fulfilling prophecy on our hands with disinflation and, ultimately, deflation becoming entrenched. In the recent collective bargaining rounds in the Austrian and German engineering sectors, there have already been indications that this process is under way, with the employers’ side using the argument of low inflation to strike very moderate wage bargains. Note that these are the strong (‘surplus’) countries. If wage bargaining goes that way in these economies, one can imagine the pressure on the bargaining position of workers in countries where prices are already falling and unemployment is sky-high.

“We are all monetarists now.” Really?

In Milton Friedman’s textbook, putting more money into the hands of economic actors prompts households and businesses to spend and invest this money, thus launching inflation or/and aggregate demand. However, instead of simply proclaiming that extra money by definition equals more spending, one should consider the concrete mechanisms through which an increase in money balances would be passed on into an increase in aggregate demand.

Here, we know that the Euro Area is very different from the US (for a more complete description and comparison, see here). In the US, QE works by pushing up the value of stocks and driving down interest rates on corporate debt. The former incites stockholders to consume more (the so -called ‘wealth effect’) whereas the latter makes it cheaper for business to finance new investment.

In the Euro Area however, these mechanisms are absent. There is no ‘wealth effect’ in the sense that households in the Euro Area do not tend to spend substantially more when their wealth increases. And businesses in Europe finance their investment mainly through the banking system and rely significantly less on direct market finance. The ECB, by pumping money into the system, will certainly boost the value of stocks and corporate debt (admittedly a major windfall gain for those that own such assets), but this will have only limited effects on aggregate spending and investment.

Unfortunately, there is more. Six years of crisis have clearly shown the consequences of heterogeneous member states sharing the same currency and an identical monetary policy. The ECB’s QE programme suffers from the same problem. Indeed, when the ECB and national central banks buy up sovereign debt according to the national central banks’ share in the ECB’s capital, €144bn of German bunds or 12.5% of outstanding German sovereign debt will be transferred to the Bundesbank and ECB balance sheets. Corresponding figures for Italy and Spain are much lower, respectively €98bn or 5% of total Italian debt and €70bn or 7.6% of Spanish sovereign debt.

In other words, the ECB’s QE represents substantial support for an economy that is already on a strong footing. One can reasonably expect QE to push interest rates on long-term10 year Bunds from their present level of 0.5% towards zero.

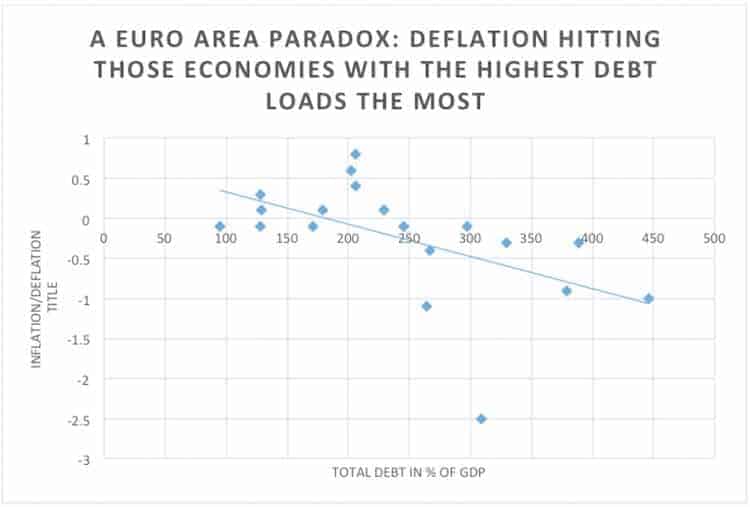

This contrasts with the troubled members of the Euro Area where, after years of recession, economic activity remains depressed, unemployment is at record highs, outright deflation has already set in and the banking system remains constrained because of a sizeable portfolio of non-performing loans (the latter being the result of austerity and economic stagnation!). And, last but not least, total debt loads, both public and private remain huge.

This paradox, whereby the ECB’s QE de facto prioritizes those member states that are in a relatively better shape, is further highlighted by the graph below. It shows that member states already experiencing deflation are at the same time saddled up with high debt loads. Given the fact that deflation increases the real burden of debt, this s is a lethal combination warranting relatively more, not less support….

QE and structural reforms: Pulling at both sides of the rope at the same time

Another shortcoming concerns whether the ECB truly understands the dynamics behind deflation.

It is indeed striking that the ECB keeps on preaching the benefits of structural reforms of labour markets, particularly that of a “radical” loosening of wage formation systems, employment protection legislation and unemployment insurance schemes. These reforms are supposed to “liberate” labour supply and boost productivity, thus getting people to spend more by raising positive expectations about their future higher incomes.

We have been here before. It is the “confidence fairy” reborn… “Confidence effects” were supposed to make fiscal austerity work. Now that this has proven not to be the case, the identical argument is used to continue with structural reforms. As if scrapping workers’ rights to a decent wage and a stable job will somehow make them feel optimistic about the future!

However, if there is one major reason why deflation is amongst us, it is the policy of structural reforms that member states adopt in pursuit of an internal devaluation of wages. Simply put: If you cut wages, prices will follow sooner or later. And if the wage squeeze is kept up long enough, disinflation will eventually end up in outright deflation.

ECB policy is therefore still characterised by a significant internal contradiction. While massively printing money to try and counter the forces of deflation, the ECB is at the same time promoting reforms that will intensify deflationary pressures even more. It is as if the ECB is pulling on both sides of the same rope at the same time. If it is really serious about fighting deflation, then that should be the priority and all policies, steering the economy in the right direction: Away from deflation, away from the ‘black zero’.

Transforming QE into a real “game changer”

These shortcomings are serious but can be met if the design of the ECB’s programme is improved.

One could, for instance, increase the volume of purchases of debt issued by European institutions and the EIB in particular. If this measure is then complemented by a bias in EIB lending towards extra public investment programmes for those countries that need it most, then a direct link between the ECB’s money printing programme and investment and job creation will be established. We can then be sure the newly printed money ends up in the real economy and in those economies that need it most.

If, on top of this, the ECB were to abandon its push for deflationary reforms of wage formation systems, then its quantum leap would stand more chances of being really successful in raising growth and inflationary expectations.