The Euro area is suffering from insufficient macroeconomic stabilisation

At the end of 2009 the unemployment rates of the Euro area and the United States had reached a level of 10%. Since then, unemployment in the US has fallen to 7.3% while in the Euro area it has climbed to 12.0%. This is not surprising as the real GDP in the United States is now 9.0% above the level of 2009, but in the Euro area it has increased by only 2.4%.

These outcomes are very closely related to very different macroeconomic approaches. The US’s fiscal policy tried to stimulate the economy with very high deficits. On average in the years 2010 to 2013, the annual US fiscal deficit was 8.7% of GDP. This is more than twice the Euro area’s deficit, which was only 4.3% of GDP. Thus, unlike the United States which made ample use of their fiscal capacity, the Euro area – especially the member countries which were most affected by the economic downturn – was forced to pursue a restrictive policy which aggravated the recession.

Different approaches can also be identified in the field of monetary policy. Almost immediately after the Lehman collapse, the FED reduced interest rates to the zero lower bound. The ECB followed a much more cautious approach. After Lehman, the ECB did not go below 1% with its own interest rate – instead it raised it again in two steps to 1.50% in July 2011. It took almost two more years before the Eurozone rate was reduced to 0.50%. The more active approach of the FED is also reflected in its quantitative easing policy. Since Draghi’s strong statement on 26 July 2012, the ECB’s bond holdings have declined from 602 billion Euros to 600 billion Euros. At the same time the FED has increased its bond portfolio from 2,472 billion Dollars to 2,844 billion Dollars.

With this in mind, the weakness of the Euro area economy cannot only be explained through structural problems. Rather, it has more to do with an insufficient macroeconomic response to a severe macroeconomic crisis. This is also reflected by a comparison with the United Kingdom which according to all indicators is the EU country with the most flexible goods, service and labour markets. Nevertheless, in order to stabilise the UK economy in the years 2010 to 2013, an average fiscal deficit of 8.0% was needed and the bond purchases of the Bank of England were even more aggressive than the quantitative easing of the FED.

Of course, the rather weak macroeconomic stabilisation in the Eurozone to a large extent reflects the specific political and institutional framework of this currency area. In contrast to the United States and the United Kingdom, the member states of the Eurozone are indebted in a currency which they cannot print under their national autonomy. This exposes them to an insolvency risk which is not the case for other developed countries such as the US, the UK or Japan. As a consequence the weaker Eurozone members were confronted with “bond-runs” of global investors in the years 2010 to 2012, which in the case of Greece, Ireland and Portugal could only be stopped by a rescue programme which required very restrictive stabilisation under the aegis of the Troika.

As far as the ECB is concerned, its ability to engage in a comprehensive quantitative easing programme in the style of the FED or the Bank of England is limited by the fact that there is no integrated market for Eurobonds. Especially in Germany, ECB purchases of bonds from individual countries are criticised as a hidden form of government financing which is prohibited by European Treaties.

Basket Eurobonds: A way to overcome the German resistance to Eurobonds

Fundamental changes to the institutional framework of the Eurozone cannot be expected for the time being. Therefore, one has to ask how better macroeconomic management could be achieved within the present legal constraints.

In the last few years, several proposals for Eurobonds or quasi-Eurobonds, such as the debt redemption pact of the German Council of Economic Experts, have been developed. But so far it has not been possible to convince German politicians and the German public that joint and several liability for Eurozone debt is required to guarantee the survival of the Euro and that the risks of such a step can be controlled. In addition, any form of joint and several liability poses serious legal challenges.

A possible way out could be a synthetic Eurobond which is designed as a basket of national bonds where each country guarantees only for its share in the basket. While such a basket-Eurobond (BEB) would be issued and traded as a single debt instrument, each participant would be liable only for the interest payments and principal redemption corresponding to its share of the bond, and not for the debt of the other issuers (Favero and Missale 2010, p. 99). Proposals for such an instrument were made already by the Giovannini Group (2000), the European Primary Dealers Association, in 2008.

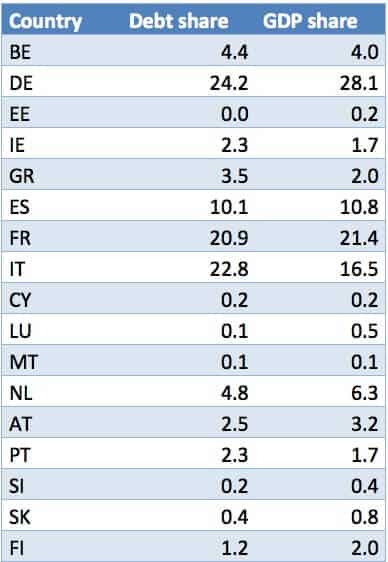

A decisive feature of such a basket-Eurobond is the share of the individual members. It could be either determined by the GDP weights of the member countries or by the share of their outstanding national government debt in total government debt of the Euro area. A basket according to debt weights would give Italy a share that is higher than its GDP share. A basket based on GDP shares would give Germany the strongest weight, while Italy’s share would be smaller than its debt share (Table 1). For the credibility of the basket-Eurobond a large German share would be more beneficial for the Eurozone. In addition, for the ECB only a Eurobond with GDP shares would avoid the criticism of implicit government financing.

Table 1: Shares of Euro area member countries in a Basket Eurobond (2012)

Basket-Eurobonds could be issued together with a sizeable issue of national bonds. Alternatively one could envisage a solution where almost all new bonds of the member states are issued as basket bonds. A large issue of basket bonds would have the advantage of a fluid market with correspondingly low interest rates. A fully developed BEB market would be much more fluid than each of the existing national markets. In addition, it would limit investor shifts from one national bond market to another, which has been a major source of instability in the last few years.

A strong expansion of the BEB market could be achieved if all new German bonds were issued as basket bonds. With a basket according to GDP shares, this would imply that countries with a debt share exceeding their GDP share (Italy, Ireland, Portugal and Greece) are forced in addition to issue a relatively small number of bonds as stand-alone national bonds. But as these countries are able to raise a very high share of the new issuance under the umbrella of the basket bond, the risk for the remaining bonds would be rather limited. In addition, if countries are obliged to issue bonds by themselves some discipline exerted by financial markets could be maintained.

For countries with a debt-to-GDP ratio below the German ratio a GDP weighted basket implies that they would raise more funds from the capital market than their funding requirement. The difference could be invested by the issuing institution (Euro Debt Agency) in assets with the same rating as the corresponding countries.

From a German perspective the main problem of a basket bond could be higher financing costs. The interest rate for the basket bond would be higher than the interest rate for a traditional German bond. This problem could be solved by differentiating the interest payments for the participants according to their individual debt levels. For instance, for each percentage point of the national debt-to-GDP ratio below the Eurozone average, a certain discount on the interest rate of the basket bond could be made. For countries with above-average debt levels a corresponding surcharge would be applied. This mechanism would provide better incentives and disincentives than the bond markets which for many years did not react to the differences in debt levels and then overreacted after the crisis had started in 2010.

The ECB’s potential for quantitative easing

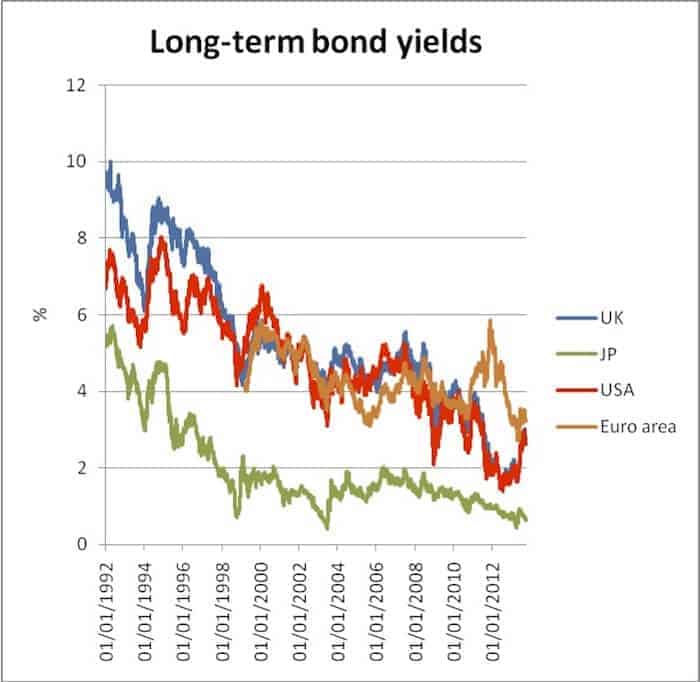

A well-developed market for Basket Eurobonds would facilitate the ECB to engage in a policy of quantitative easing in the same way as central banks of other major currency areas. With an explicit commitment by the ECB to purchase a certain number of basket bonds for an extended period of time, the average long-term interest rate of the Eurozone could be reduced. Since the outbreak of the financial crisis, this rate has been considerably higher than long-term bond yields of other major currency areas (see chart). Fundamentally this spread is not warranted as the average deficit of the Eurozone has been lower than the deficit of other major currency areas. At the same time, the Eurozone debt level has been more or less identical to the US and the UK level, but much lower than the Japanese level.

Of course, since July 2012 the ECB’s Outright Monetary Transaction (OMT) announcement has already helped to reduce the average interest rate considerably. But there is a risk that this commitment could be tested and that the ECB’s purchases of national bonds could be limited by legal concerns. With purchases of BEBs the ECB could always argue this is a purely monetary operation as it does not favour individual countries.

At the moment the ECB’s bond holdings amount to 6.3% of the Eurozone’s GDP, the FED’s bond holding total 17.5% of GDP. The monthly gross issuance of government bonds of Eurozone member countries is about 200 billion Euros. Thus, after the establishment of BEBs the ECB could announce monthly purchases of 50 billion Euros for a 12 month period. The total amount of 600 billion Euros would be equivalent to about 6% of the Eurozone’s GDP. It would double the ECB’s bonds holdings and help reduce the average Eurozone bond rate, as it will take the same time until a major number of BEBs become available. The ECB could start its OMT programme by purchasing national bonds according to the GDP weights of the member states.

Of course, the implementation of a BEB would raise a host of technical questions, above all concerning the legal status of the Euro Debt Agency, the timing of issues and the maturity of the BEBs. Nevertheless, BEBs are the only form of Eurobond which do not require joint and several liability and they are therefore the only instrument that can be implemented within the current institutional framework.

Hope for the unemployed

In spite of some positive signals the overall economic situation of the Eurozone is still rather bleak. The HICP inflation rate is now only 1.1% which is almost in a deflationary terrain as it is below the ECB’s target of close to 2%. Although the IMF expects a return to growth in the Eurozone in 2014 and growth rates of about 1.5% in the following years, the Euro unemployment rate will increase to 12% in 2014 and will remain above 11% until 2017.

Of course, structural reforms can be helpful to improve the competitiveness of the Euro area. But without a dynamic macroeconomic environment, improvements at the microeconomic level will not materialise. Under the current legal framework, the fiscal space of the Eurozone member states will remain very limited. Therefore, the ECB will remain the only powerful actor at the macro level. Its commitment to OMT has already shown a remarkable impact on financial markets. With the issuance of basket Eurobonds the ECB’s ability to engage in a policy of quantitative easing could be significantly improved. In addition purchases of such bonds could no longer be criticised as a form of implicit government financing.

References

European Primary Dealers Association, Securities Industry and Financial Market Association (2008), A Common European Government Bond, Discussion Paper, September 2008

Favero, C.A. and A. Missale (2010), EU Public Debt Management and Eurobonds, European Parliament Directorate General for Internal Policies

Giovannini Group (2000), Co-ordinated Public Debt Issuance in the Euro Area.