Economic recovery in the Eurozone is not delayed. It is non-existent. The Financial Times for the first day of October carried several articles assessing the European economies, written as if a prize would go to the most pessimistic — stagnation and decline of EU manufacturing, the European Central Bank initiates asset purchases to prevent deflation from sweeping the continent, France and Italy sure to miss their fiscal targets, and the head of the IMF warns of global economic “mediocrity”. And, as the comics say, that’s the good news.

The reason for this dismal economic performance is an oft-told-tale. The relentless pursuit of fiscal cuts, “austerity”, depressed aggregate demand across the EU, turning a transitory financial collapse into a depression-generating disaster. As four consecutive years of budget cutting madness have created a gathering human disaster, the German government presses for yet more Commission powers to prevent any EU member government from coming to its senses and abandoning these scorched earth macro policies (the TSCG Treaty mandating “balanced” budgets and the monitoring & surveillance SixPack, with more to come).

The instigators of these anti-social and anti-democratic policies, rules and treaties defend them as the mechanisms to bring recovery, end fiscal deficits and reduce public indebtedness. Were they successful, their authoritarian nature should make them unacceptable in any democratic country. They allow unelected EC officials to over-ride decisions of elected national parliaments.

The rules and regulations to enforce austerity have achieved no purpose other than to undermine the democratic process in Europe. Austerity has not brought recovery. It has not brought fiscal balances below the famous Maastricht 3% limit. Nor have public debts come close to achieving that other Maastricht fiscal fantasy, a debt to GDP ratio of 60% or less. There is one exception to this litany of folly — Germany. Its success and the failures of other countries are part of an interrelated package.

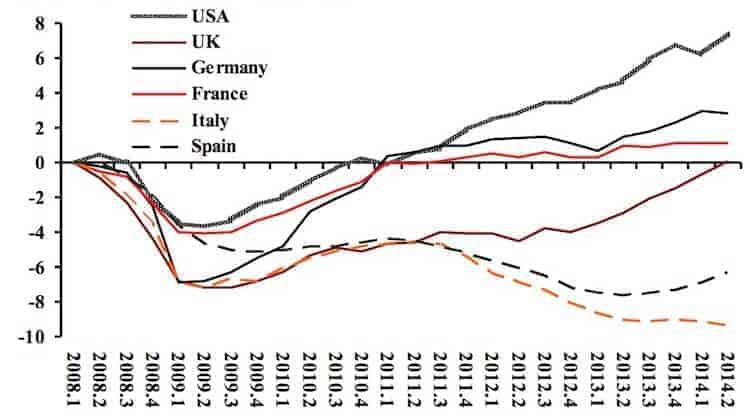

The chart below shows the dismal growth performance of the United States and the five largest EU countries. By comparison, the US recovery looks good: 8% above the pre-crisis peak in the first quarter of 2008 (after six years!). The best the EU could produce among the five largest countries is the anemic 3% for Germany in the first quarter of 2014 (and slightly less, 2.8%, in the second quarter). The French economy staggers in at a meager 1% for the second quarter, unchanged from a year before, while the UK barely returned to where it was a full six years before.

Italy and Spain, whose governments embraced the ideology of fiscal “consolidation”, languish far below the pre-crisis peak. Were it not for the catastrophic collapse of the Greek economy under the weight of EC imposed fiscal contraction, Italy and Spain would be recognized as unmitigated disasters. Since the end of World War II no major country has suffered declines as deep and prolonged as have Italy and Spain. A cyclical growth pattern characterizes all market economies. Prolonged stagnation does not. This must be self-imposed through growth-depressing policies — aka, austerity.

USA and the 5 Largest EU countries, percent difference in output compared to first quarter of 2008

Note: Each point on a country’s line shows percentage difference from 2008.1, which is set to zero. The source is www.oecd.org.

Fiscal deficits decline and turn into surpluses as a result of economic growth, not cuts in public expenditure. If anyone requires proof of this assertion, the performance of the US and EU fiscal balances since 2008 provides it. In 2007 the five largest EU countries all had overall fiscal balances at or above the Maastricht minus 3% limit (with the US deficit slightly above 3%). Two years later not one of the EU five could claim the arbitrary Maastricht rule (Germany came closest at 3.1%).

These superficially shocking fiscal deficits had two principle causes, the sharp fall in public revenue due to declines in corporate and household income, and re-financing of commercial banks that teetered on the verge of collapse. The largest reversal was for Spain, from a 2% surplus in 2007, to an 11% deficit in 2009. About half of the reversal of the Spanish balance represented replenishing commercial bank reserves, not expenditure in the usual meaning (i.e., increasing aggregate demand).

Only one of the five EU countries experienced a substantial and sustained reduction of the overall fiscal deficit, Germany. One other country made it under the infamous 3%, Italy. Like Germany, this is an exception that proves the rule that cuts are not an effective policy to reduce deficits. At its most negative the Italian deficit was 5.4%. This declined to marginally below minus 3% before the various Italian governments embarked on “fiscal consolidation”.

USA and the 5 Largest EU countries, overall fiscal deficits as share of GDP, 2007-2014 (dashed line is the Maastricht 3% limit)

Source: www.oecd.org. The 2014 value is the annual equivalent of the first 2 quarters.

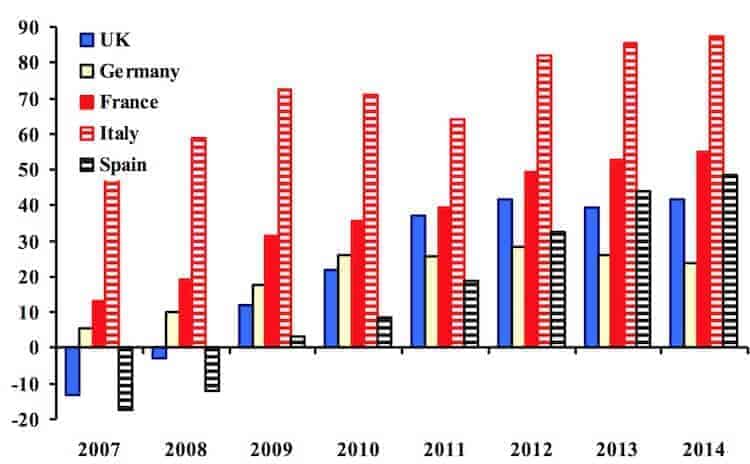

The performance for public debt is even worse than for deficits. The chart below shows the difference between the actual debt to GDP ratio and the Maastricht 60% rule. Most commentators would identify 2010 and the Greek crisis as the beginning of de facto commitment to fiscal contraction. This coincides with the election of the right of center coalition government in Britain and the enthusiastic implementation of its own version of the austerity ideology.

Since 2010 in only one country do we find a decline in the public debt to GDP ratio, again Germany. Even in this case the decline is meager, from 26 percentage points above the Maastricht limit in 2010, to 24 above in 2014. The UK ratio shows a similar story, hardly changing during 2011-2014. For France, Italy and Spain we see a relentless increase in the public debt ratio from 2010 onwards.

The 5 Largest EU countries, public debt to GDP ratio, less the Maastricht 60%, 2007-2014

Source: www.oecd.org. The 2014 value is the annual equivalent of the first 2 quarters.

Attempting to reduce fiscal deficits through expenditure reduction is an ideologically driven project doomed to failure. By depressing public expenditure when it is most needed to stabilize aggregate demand austerity policies provoke stagnation. The stagnation in output prevents recovery of public revenue. The austerity ideologues seek to obscure the sane economics of public finances by invoking voodoo concepts such as “structural deficits” (see critique in Chapter 7 of my new book) and “expansionary austerity” (the IMF debunked this in a 2011 working paper).

Economic recovery of the European Union as a whole and especially the Eurozone awaits a fundamental change in policy from punitive austerity to growth-stimulating fiscal expansion, a shift endorsed in the October issue of the IMF’s World Economic Outlook. Without a shift, the famous one liner attributed to rural inhabitants of the US state of Maine applies to EU recovery, “you can’t get there from here”.