It looks like Greece may get some debt relief. There is as yet no certainty about this because some German politicians continue to conduct rear-guard battles to prevent it. What is certain, however, is that all Eurozone countries, with the exception of Greece, have been enjoying debt relief since early 2015. That may seem surprising to the outsider. Some explanation is necessary here.

QE as EZ debt relief: But not for Greece

As part of its new policy of ‘quantitative easing’ (QE), the ECB has been buying government bonds of the Eurozone countries since March 2015. Since the start of this new policy, the ECB has bought about €645 billion in government bonds. And it has announced that it will continue to do so, at an accelerated monthly rate, until at least March 2017 (Draghi and Constâncio 2015). By then, it will have bought an estimated €1,500 billion of government bonds. The ECB’s intention is to pump money in the economy. In so doing, it hopes to lift the Eurozone economy out of stagnation.

I have no problems with this. On the contrary, I have been an advocate of such a policy (De Grauwe and Ji 2015). What I do have problems with is the fact that Greece is excluded from this QE programme. The ECB does not buy Greek government bonds. As a result, the ECB excludes Greece from the debt relief that it grants to the other countries of the Eurozone.

How is this possible? When the ECB buys government bonds from a Eurozone country, it is as if these bonds cease to exist. Although the bonds remain on the balance sheet of the ECB (in fact, most of these are recorded on the balance sheets of the national central banks), they have no economic significance anymore. Each national treasury will pay interest on these bonds, but the central banks will refund these interest payments at the end of the year to the same national treasuries. This means that as long as the government bonds remain on the balance sheets of the national central banks, the national governments do not pay interest anymore on the part of its debt held on the books of the central bank. All these governments enjoy debt relief.

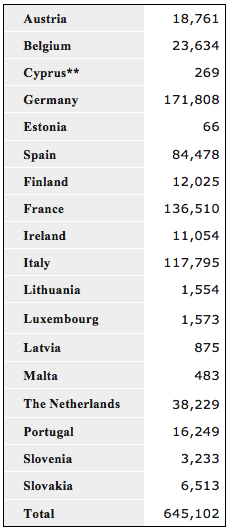

How large is the debt relief enjoyed by the governments of the Eurozone? Table 1 gives the answer. It shows the cumulative purchases of government bonds by the ECB since March 2015 until the end of April 2016. As long as these bonds are held on the balance sheets of the ECB or the national central banks, governments do not have to pay interest on these bonds. The ECB has announced that when these bonds come to maturity, it will buy an equivalent amount of bonds in the secondary market. We observe that the total debt relief granted by the ECB until now (April 2016) to the Eurozone countries amounts to €645 billion. We also note the absence of Greece and the fact that the greatest adversary of debt relief for Greece, Germany, enjoys the largest debt relief from the ECB.

The announcement of the ECB that it will continue its QE programme until at least March 2017 and that it will accelerate its monthly purchases (from €60 billion to €80 billion a month) implies that the debt relief that will have been granted in March 2017 will have more than doubled compared to the figures in Table 1. For many countries, this will amount to debt relief of more than 10% of GDP.

Table 1 Cumulative purchases of government bonds (end of April 2016)

(million euros)

Source: ECB (for details on the ECB’s asset purchase programmes, see see here).

Greece is excluded from the QE programme, and thus from the debt relief that arises as a result of this programme. The ECB gives a technical reason for this exclusion: Greek government bonds do not meet the quality criteria required by the ECB in the framework of its QE programme. But that is extremely paradoxical. Countries that have issued ‘quality’ bonds enjoy debt relief. As soon as they are on the central banks’ balance sheets, these bonds cease to exist from an economic point of view. It is as if they are thrown in the dustbin. Thus this whole operation amounts to throwing the good bonds in the dustbin, but not the bad bonds.

The exclusion of Greece is not the result of some unsurmountable technical problem. These technical problems can easily be overcome when the political will exists to do so. The exclusion of Greece is the result of a political decision that aims at punishing a country that has misbehaved.

It is time that the discrimination against Greece stops and that a country struggling under the burden of immense debt is treated in the same way as the other Eurozone countries that have been enjoying silent debt relief organised by the ECB.

References

De Grauwe, P. and Y. Ji (2015), “Quantitative easing in the Eurozone: It’s possible without fiscal transfers”, VoxEu.org, 15 January.

Draghi, M. and V. Constâncio (2015), “Introductory statement to the press conference (with Q&A)”, 3 December.

This article originally appeared on VOX.