Macroeconomics is a sick science. It suffers from the fact that it largely suppresses a great scientific revolution to this day.

Copernicus discovered that the laws of motion of the sun and the earth were quite different from what was represented in Ptolemy’s world view. Imagine if astronomy had drawn the conclusion that in the short term the earth rotated around the sun but in the long term the earth would still be at the centre of the universe. Yet that is exactly what happened in economics after the Keynesian revolution.

John Maynard Keynes made a discovery as fundamental as that of Copernicus. He recognised that the laws of motion conceived by classical economics were wrong. He wrote in the very first paragraph of The General Theory of Employment, Interest and Money:

I shall argue that the postulates of the classical theory are applicable to a special case only and not to the general case … The characteristics of the special case assumed by the classical theory happen not to be those of the economic society in which we actually live, with the result that its teaching is misleading and disastrous if we attempt to apply it to the facts of experience.

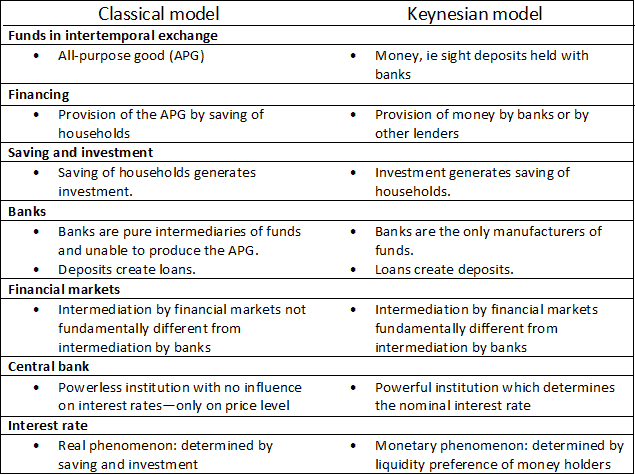

Indeed, the laws of motion of the classical and the Keynesian world view differ, as set out in the figure below. In the classical model saving generates investment. In the Keynesian model investment generates saving. In the classical model saving and investment determine the interest rate. In the Keynesian model saving and investment determine aggregate output.

But unlike in astronomy, this scientific revolution was successfully defeated by the classical paradigm. The representatives of the old regime carried this off with a brilliant move. They developed the ‘neoclassical synthesis’, turning the tables by presenting the Keynesian world view instead as a special case of the classical.

Whereas Keynes had contended in The General Theory that the ‘postulates’ of classical theory only operated in the exceptional case of full employment, the neoclassicals argued that the Keynesian laws of motion were only valid in the situation of rigid prices—and so in the short term. In the long term, with flexible prices, the laws of motion of the classical model would still apply.

It remained largely open, however, why the laws of motion of the economy could differ so fundamentally between regimes of rigid and flexible prices. Take saving and its influence on interest rates and investment.

In the classical model, household saving is the decisive precondition for investment. A higher propensity to save increases supply on the capital market, so that the interest rate falls and the investment volume rises.

In the Keynesian model, however, increased household saving leads to lower demand for goods. In the financial sector, lower household spending leads to higher household money holdings and lower corporate money holdings. The money supply in the economy remains constant, so that there is no interest-rate effect.

Financial system

Is this fundamental difference between the two models due to the flexibility or the rigidity of prices? The explanation lies rather in the different modelling of the financial system.

In the classical modelthere is no money. There is only one all-purpose good which can be used equally as a consumer good, an investment good and as a means of finance (‘funds’). In this model, saving—not consuming the all-purpose good—is the prerequisite for investment. Basically, the classical model is a model for a corn economy: households decide whether to consume the corn or to save it. If it is saved it can be supplied to investors who sow the grains, repaying to the households one period later the credit amount plus interest.

In the Keynesian model the ‘funds’ exchanged on the capital market are made up of money—‘funds’ are bank deposits. Funds are not created here by a renunciation of consumption but by the banks granting credit.

The classical model is therefore not a representation of the long-term laws of economic motion. It is the representation of a fantasy world whose laws of motion have nothing to do with reality. With these opposite laws of motion, a synthesis of the classical and the Keynesian model is as flawed as an attempt to combine the models of Ptolemy and Copernicus. In fact, Tycho Brahe (1546-1601) tried a similar synthesis (the Tychonian system) but, of course, it failed.

Reputational damage

For economics as a science, the neoclassical synthesis has led to huge reputational damage. Its inability to recognise the Great Financial Crisis (GFC) is due to the fact that in the classical model the role of banks is reduced to that of mere intermediary between savers and investors. Banks are unable to create the all-purpose good that is constitutive for this model.

In the Keynesian model, by contrast, banks do not need deposits for lending. They can create money on their own, which, if not sufficiently controlled by banking supervision, can lead to excessive lending. This is exactly what happened in the years before the GFC. Thus, when Queen Elizabeth asked LSE economists after the crisis, ‘If these things were so large, how come everyone missed them?’, the correct answer would have been: ‘Because in our analyses of the financial system we use models without money.’

After this painful experience, it is almost incomprehensible that the classical paradigm is not only presented uncritically in the leading textbooks but also shapes modern macroeconomic models: banks, if they exist at all, are still reduced to the role of mere intermediary. A recent survey describes the state of the art as follows:

… even when banks are included, their treatment is highly stylised. For example, many models simply assume the presence of banks, but do attempt to justify their existence …

The failed revolution also has far-reaching economic-policy implications. In the classical model, there is a strict crowding out of private investors on the capital market by government deficits. The all-purpose good, which functions equally as ‘funds’ and as investment good, can only be used once.

In the Keynesian model, on the other hand, ‘funds’ (money) and investment goods are independent of each other. Therefore there is no crowding out on the capital market, if deficits are financed by banks or the central bank. This is the fundamental insight of Modern Monetary Theory.

How can the Keynesian revolution be completed? The chances of achieving this today are not very good, because to do so would devalue the human capital of most macroeconomists. Thus, young students need to wake up and realise they are being taught models whose laws of motion are as inconsistent with reality as Ptolemy’s world view. We need a ‘Fridays for Keynesianism’ movement.

This article is a joint publication by Social Europe and IPS-Journal