Six months ago, I wrote a column for Social Europe with the title ‘Coronavirus crisis: now is the hour of Modern Monetary Theory’. While I think it is unlikely that the economists of the US government and the Federal Reserve read it, they seem to have come up with the same idea. In any case, the monetary and fiscal policies which have been pursued in the United States over the past six months are perfectly in line with the recipes of Modern Monetary Theory (MMT).

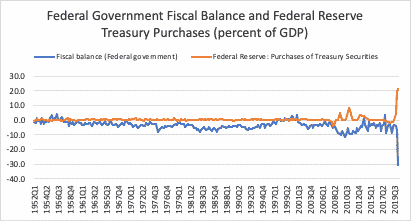

Let’s start with fiscal policy. In the second quarter of 2020 the federal government’s fiscal balance reached -30.2 per cent of gross domestic product. This value by far exceeds the previous quarterly record deficit of 11.6 per cent, in the second quarter of 2010. What did the government do with all the money? A large amount was used for transfers to private households. The Coronavirus Aid, Relief, and Economic Security (CARES) Act, enacted in March, gave the unemployed an extra $600 a week in benefits. This supplement played a crucial role in limiting extreme hardship; poverty may even have gone down.

What about monetary policy? In line with MMT the Fed started already in the first quarter to purchase huge amounts of Treasury securities. In a longer-term perspective the amount of these transactions far exceeded any historical precedent. During the ‘quantitative easing’ period in the first quarter of 2011, the Fed purchased a maximum amount of Treasuries, totalling 8.4 per cent of GDP. In the first quarter of 2020 the purchases reached 18.9 per cent and 21.2 per cent in the second quarter (see graphs).

While MMT envisages direct central-bank lending to the government, the Fed typically purchases bonds on the secondary market from primary dealers—large, globally active banks. But if the banks know that the Fed is willing to purchase, in effect, unlimited amounts of Treasuries, this does not make an economic difference.

Immediate impact

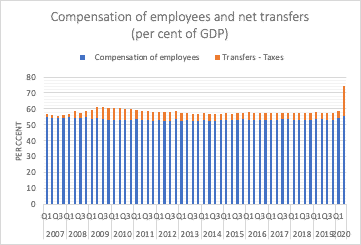

What were the economic effects of this strategy? It had an immediate impact on disposable personal income—again, way beyond any precedent. Net transfers (after tax) reached almost one-fifth of GDP; in the Great Recession the maximum was 7.5 per cent, in the first quarter of 2010. Thus, the transfer payments did not only compensate for the decline in wage incomes: they boosted the disposable incomes of American households to a record high (see bar chart).

What did households do with all the money? Due to the coronavirus-related restrictions in the second quarter, they nevertheless reduced their consumption significantly. Their disposable income in the second quarter was $1.6 trillion (on an annualised basis) higher than in the fourth quarter of 2019 but their consumption expenditures declined by $1.8 trillion. As a consequence, the personal saving rate also reached a record high of 25.8 per cent; the previous record was 17.3 in May 1975. This boosted the growth rate of the money stock M1, which increased by 27 per cent from the fourth quarter of 2019 to the second quarter of 2020.

All in all, with these extreme changes of important macroeconomic variables one can definitively say, as Gita Gopinath has put it, that the pandemic is ‘a crisis like no other’.

Induced coma

The key question is whether the MMT ‘bazooka’, to use the wording of the German finance minister, Olaf Scholz, for his first stimulation package, was successful. Given the induced coma of the whole economy caused by the pandemic regulations, especially in April and May, it is not surprising that in the US a decline of GDP by 9.1 per cent (non-annualised) proved unavoidable and that unemployment soared to 14.7 per cent in April.

But from today’s perspective the assessment is not so bad. Above all, 11 million people in the payroll survey have gone back to work, out of 22 million who lost their jobs in March and April. At a press conference on September 16th, the Fed chair, Jerome Powell, made the following statement:

I guess I would start by saying that the initial response from fiscal authorities was rapid. It was forceful and pretty effective. And we’re seeing the results of that today in income and household spending data, in the labor market data, in the construction data, in the data for business equipment spending, and the fact that businesses are staying in business, and you know, the pace of default and things like that has really slowed. So there’s been a really positive effect.

What about the inflation risks of MMT? For monetarists (who believe inflation is caused by increases in the money supply, whereas Keynesians associate it with distributional conflict), the massive increase in the money stock is definitely a matter for concern. But for the time being the US economy will show a major negative ‘output gap’, indicating scope for non-inflationary expansion. Thus, when households gradually reduce their unusually large bank balances, this should not lead to inflationary pressures.

It is too early for a comprehensive evaluation of the MMT strategy practised by the US government and the Fed in the past six months. But it is surprising that famous US economists who dismissed MMT—such as Larry Summers (‘recipe for disaster’), Paul Krugman or Kenneth Rogoff (‘Modern Monetary Nonsense’)—have so far not criticised the joint fiscal- and monetary-policy response to the economic consequences of the pandemic. Indeed, Krugman even praised the CARES act and called for its extension.

As the end of World War II approached, the British prime minister, Winston Churchill, is reputed to have said: ‘Never waste a good crisis.’ For economists the extreme fluctuations of key macroeconomic variables caused by the coronavirus crisis, and the attempts to deal with it, provide a fascinating object of analysis and the chance to gain new insights into macroeconomic processes.

So, for example, prominent economists may believe that household ‘savings’ finance government debt, which it is then implicitly shameful for governments to increase. Yet the crisis clearly shows that it is government debt, financed by the financial system—and so the central bank—which generates private saving.

This article is a joint publication by Social Europe and IPS-Journal