The Covid-19 pandemic has led to an enormous slump in economic activity worldwide. At the same time, fortunately, governments and central banks have implemented economic stimulus measures unprecedented in economic history. With such a combination of massive shock and very highly dosed therapy, the question increasingly arises as to whether this will result in inflationary or deflationary trends for the global economy in the medium term.

Particularly in the German discussion, there is increasing concern about the possible inflationary effects of the stimulus measures. Hans-Werner Sinn, longstanding president of the prestigious ifo-Institute and one of the best-known German economists, is already drawing parallels with domestic hyperinflation in the first half of the 1920s.

Three phases

For an analysis of the economic effects of the coronavirus pandemic it is useful to distinguish three phases:

- Phase I—comprehensive lockdown, as practised in Europe from March to May;

- Phase II—the ‘new normal’, in which above all sometimes very strict curfews have been lifted and, subject to restrictions, purchases at retail stores or availing of services such as restaurants and travel are once again possible.

- Phase III—the ‘true normal’, when the virus is effectively brought under control and social life can return to its pre-pandemic level.

In phase I, the coronavirus crisis proved a simultaneous supply and demand shock. International supply chains were disrupted. Many workers had to look after their children due to the closure of kindergartens and schools. In some countries, economic activities were suspended almost completely.

On the demand side, the lockdown at this stage meant consumers were no longer able to demand certain services (‘social consumption’). Travel and all related services came almost to a standstill.

The impact of these shocks on prices can already be seen: in the United States, the consumer-price index fell by 1.3 per cent in seasonally adjusted terms from February to May, in the euro area by 0.7 per cent. If the price effects of the demand shock have thus been stronger than those of the supply shock, this is mainly due to the sharp decline in energy prices, as unprocessed food has become more expensive.

Anything but normal

The ‘new normal’ which has now emerged in Europe is anything but normal. Supply-side constraints are losing their importance, although the sustained need for distancing continues to have a negative impact on productivity in both industry and services. On the demand side there remains a strict ban on large-scale gatherings (concerts, congresses, sporting events). Rising unemployment is also having a negative impact on overall economic demand, as is the short-time work (Kurzarbeit) practised particularly in Germany (and Austria), which is also leading to a decline in net incomes.

In addition to these direct effects, overall economic demand is likely to suffer from the great uncertainty about the progress of the pandemic, especially the danger of a ‘second wave’. This will lead to postponement of corporate investments, as of the purchase of cars or other longer-term consumer goods by households. Overall, the price-dampening demand effects will likely dominate the price-driving supply effects even more than in phase I.

The phase of ‘true normal’ will only be reached when it is possible to find a vaccine against the coronavirus and/or an effective therapy for its victims. With the return to a normal social life, the restrictions on supply should lose much of their significance. Demand is however likely to continue to suffer from the many job losses, while with many corporate balance sheets massively damaged by the crisis, the scope for financing investments will remain severely restricted.

‘Debt brake’

To combat the crisis, all countries have increased government spending and reduced taxes. Together with the ‘automatic stabilisers’—such as welfare spending rising with unemployment and offsetting demand loss—this has led to high deficits and a sharp rise in public debt. In general, the need to consolidate public debt should lead to a rather restrictive approach to fiscal policy. In Germany, there is even a legal obligation to reduce the national debt incurred in the course of the crisis—the ‘debt brake’ (Schuldenbremse) enshrined in the German constitution in 2009.

In this subdued environment, it will be difficult for the trade unions to push for significant wage increases. Since inflation rates have already been very low by historical standards in the past decade—given a relatively robust economic and labour-market situation—it is therefore highly unlikely that the crisis will lead to strong upward pressure on prices in phase III as well.

On the whole, there is a greater risk that the pandemic will lead to deflation in the global economy. Experience gained since March 2020 may lead to a fundamental change in our attitudes towards mobility. Intensive use of the home as office will lead to a reduction in trips to work and lower demand for cars and office space. Travel to workshops and conferences will be significantly reduced, to the detriment of airlines, hotels and restaurants. As a result, energy prices will remain permanently low as demand for oil declines.

The deflationary effects will be all the more noticeable to the extent that it is impossible in phase II to avoid a rise in unemployment and a widespread wave of insolvencies. For large economies such as the US, Japan and Germany, this is much easier to achieve than for smaller and sometimes highly indebted cases such as Italy, Greece or Spain.

Hyperinflation scenarios

From where then do German inflation-phobes derive their hyperinflation scenarios? Sinn cites the sharp rise in the monetary base in the eurozone:

The amount of money put into circulation by the central bank was 1.2 trillion euros before the euro crisis broke out. At the end of last year, it was already at 3.7 trillion euros, and after the measures already adopted, it is expected to reach 4.8 trillion euros by the end of the year.

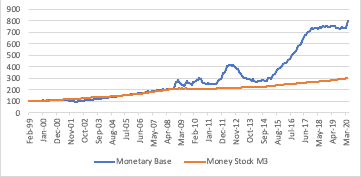

If one puts these numbers into a simple quantity equation—which explains the price level by the money supply, its velocity of circulation and the quantity of goods—one can easily conclude that sooner or later large-scale inflation will follow. But the money put into circulation by the central bank (the ‘monetary base’) is an aggregate, which in the euro area comprises, according to April 2020 data, around one-third cash in circulation (€1.3 trillion) and some two-thirds banks’ balances with the central bank (€2.2 trillion). This aggregate is irrelevant to the spending behaviour of households and enterprises. The money that matters is the money stock ‘M3’, which is composed of bank deposits (€12.3 trillion) and the currency in circulation (€1.3 trillion).

The monetary base has indeed risen very strongly over the past decade, as shown by Sinn. But this expansion of banks’ balances at the central bank was brought about by European Central Bank bond purchases. These have had a very limited impact on the money holdings of non-banks, which only rose at a rate of 3 per cent per annum between 2008 and 2019 (Figure 1).

Figure 1: euro-area trends (February 1999 = 100) in money stock (M3) and the monetary base

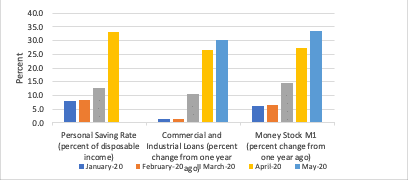

There has however been an unusual recent acceleration in the growth of non-bank money holdings, particularly apparent in the US. The money stock ‘M1’ (cash and easily convertible equivalents) now shows a year-on-year growth there of 33.5 per cent. This money creation is related to a similarly strong increase (30.3 per cent) in bank loans to enterprises (Figure 2).

Figure 2: the personal saving rate and annual growth rate of commercial and industrial loans and the money stock (M1) in the US

The underlying problem is an unprecedented increase in the household saving rate as a proportion of disposable income, which stood at 33.0 per cent in April. The sharp rise in money holdings therefore reflects the increased holdings of households which stopped spending and the need for companies to replace lost revenues with bank loans. None of this is indicative of inflationary risks—rather, of significant deflationary risks.

By the way, this nicely shows that household saving is—in contrast to the classic theory—not a blessing but a curse for the economic system.

This article is a joint publication by Social Europe and IPS-Journal