A fierce debate is raging about European macroeconomic policy.

German media increasingly attack the ultra-loose monetary policies of the European Central Bank (ECB), in defence of prudent savers, while former and current central bankers have criticised further unconventional easing. Beyond monetary hawks pushing for tight money, fiscal orthodoxy is resisting calls for loosening purse strings: the German government is reluctant to deviate from its schwarze Null policy of balanced budgets.

Additionally, core eurozone countries reject more risk-sharing among members of the currency union. They claim loose money and budgets would just ‘let profligate countries off the hook’, encouraging further irresponsible behaviour.

Europe’s excess saving

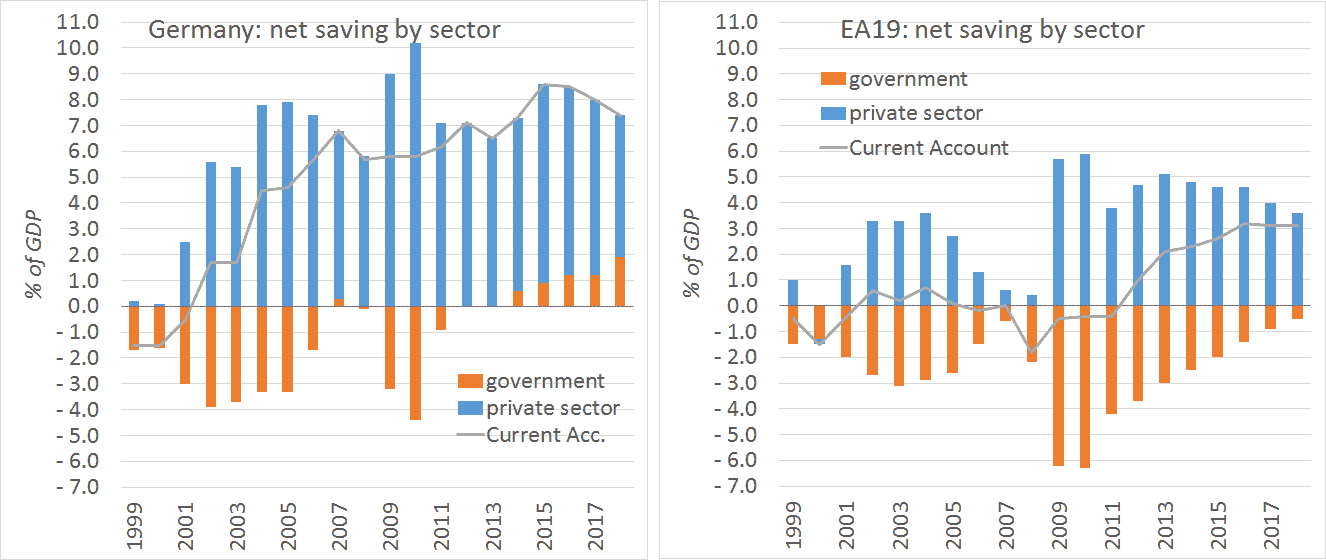

The propensity to save has risen significantly in the euro area. This is partly due to more private-sector saving in Germany, driven by redistribution through suppressed wages from labour to rich capital owners (who save more), and partly to the large deleveraging pressure and fiscal austerity imposed on the euro periphery after the financial crisis (see charts below).

At the macro-level, for somebody to save, there must be someone else to borrow. This means that a rise in private saving propensity must be: A) discouraged by lower real interest rates, which also stimulate private borrowing / investment demand, B) offset by fiscal deficits and public borrowing or C) channelled abroad via current account (CA) surpluses (essentially by lending to foreigners).

If none of the above happens, rising saving propensity manifests itself in a fall in overall spending. Since one person’s spending is another’s income, this means incomes must fall, leading to higher unemployment (illustrating Keynes’s ‘paradox of thrift’).

Monetary stimulus

To avoid rising unemployment and to support aggregate demand, the euro area engineered an extensive monetary stimulus (channel A). The ECB has cut short-term nominal interest rates below zero, and further lowered long-term rates via ‘quantitative easing’ (QE).

Granted, lower returns on their deposits do not represent great news for savers but this is precisely the point—to discourage excessive saving. Putting up with a smaller interest income is most likely preferable to the alternative of losing a job (certainly for those without savings).

In any case, blaming the ECB makes little sense, as lower equilibrium real interest rates are caused not by the central bank but by excessive saving itself. Keeping or raising actual policy rates above the equilibrium rate wouldn’t solve the underlying problem of excess saving but rather exacerbate it: spending would be depressed, hurting the very incomes from which saving is possible, resulting in higher unemployment as demand is weakened.

Fiscal-policy role

Due to the zero-lower-bound (ZLB) constraint, however, the ECB failed to reduce interest rates enough. With monetary policy out of firepower, central bankers and macroeconomists increasingly call for a larger role for fiscal policy (channel B) in cyclical demand stabilisation at the ZLB.

This entails more flexible fiscal rules in the eurozone, as well as a clearer monetary backstop role for the ECB in public debt markets to accommodate the necessary fiscal expansion. In the absence of such reforms, enabling better monetary-fiscal co-ordination, euro periphery governments were unable to maintain persistent fiscal support and had to undergo harsh austerity during the crisis.

Alternatively, governments such as Germany’s, constrained neither by the EU’s fiscal rules nor by financial markets, should wield their fiscal firepower in support of aggregate demand. Although this leads to higher budget deficits and public debt, it is precisely this extra public borrowing which can soak up the rise in private savings. In contrast, Germany increased its primary budget surpluses, further contributing to excess saving, putting further downward pressure on interest rates.

Wishing for higher interest rates will therefore not work together with a push for continued government debt reduction. If the priority remains primary fiscal surpluses and schwarze Null, then its advocates must accept that this world of excess saving entails ultra-low real returns for savers and monetary policy stuck at the ZLB. They cannot have it both ways.

Current-account surpluses

German policy-makers can counter that even without monetary or fiscal stimulus they still have the third option, relying on foreign demand (channel C). Indeed, Germany’s excess saving over its domestic investment is mirrored in its large and persistent current-account surpluses, which reflect lending to foreigners. The problem with this, however, is that it relies on foreigners’ willingness to spend and run the corresponding CA deficits.

Moreover, running CA surpluses in a global liquidity-trap environment (where interest rates cannot fall any further and cash is hoarded) is a zero-sum game: it captures already scarce demand from trading partners, unleashing deflationary forces elsewhere. It is precisely why Keynes proposed that in a world of excess saving surplus countries should bear more of the burden of CA rebalancing by spending more, instead of forcing deficit countries to save more.

A German fiscal boost could have eased the balance-of-payments adjustment of the periphery during the euro crisis, saving them from painful debt-deflation and unemployment. While this assumes some degree of risk-sharing, if the euro is to work Germany cannot shun this responsibility.

Not prudence, folly

In any case, relying on fiscal stimulus instead of running CA surpluses is not a sacrifice in the interests of others: it would also benefit Germany. A well-designed package could improve long-term growth through public investments and raise wages, improving German households’ living standards, while reducing inequality. It would be affordable at current ultra-low interest rates and would provide much needed safe assets.

The ECB under its former president, Mario Draghi, arguably saved the eurozone from disintegration and depression with his ‘whatever it takes’ monetary stance. Instead of assigning blame, it should be applauded. The fiscal dogma of schwarze Null is not prudence but folly. It hurts Germany as well as Europe and should be abandoned.